Share This Post Today!

Gatteville Lighthouse, Gatteville-le-Phare, France

This lighthouse was built in 1834 in the Normandy region of France. The 247-foot-tall lighthouse is the 3rd tallest traditional lighthouse in the world. The light station was established in 1774 due to strong currents and many shipwrecks occurring in the area.

Chipiona Lighthouse (Punta del Perro Light), Cadiz, Spain

This lighthouse is located on the south-west coast of Spain close to Portugal. The lighthouse was first lit in 1867.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

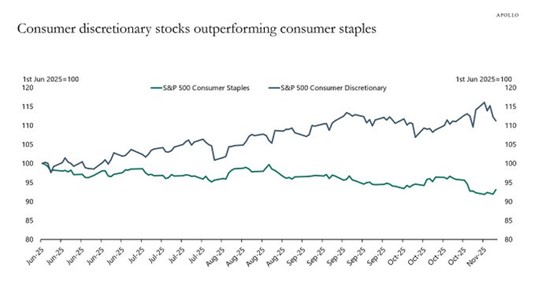

2025: the year of the K-shaped economy

As 2025 has unfolded, we have mentioned the breakdown of economic conditions, yet markets continue to move higher. Both inflation and the job market are showing real problems. Loan defaults have crept up, interest rates remain elevated, and consumer balance sheets are deteriorating. So, how do markets and investors justify buying stocks at all-time highs at 40 times earnings? Easy, high-growth growth and discretionary names continue to move higher while certain staples struggle. This is the result of a K-shaped economy. Two different groups are facing polarizing economic conditions that continue to deteriorate from one another.

Apollo recently released a study examining the K-shaped economy. Here is a chart that describes this phenomenon:

Over the last few months, many staples on the S&P 500 have moved lower on weak outlooks, earnings misses, and elevated macro risk factors. At the same time, discretionary names have moved higher. The explanation: higher-income households are not facing the same economic problems that the middle and lower classes are facing. This strength of high-income household balance sheets, relative to lower-income balance sheets, is a driver of the K-shaped economy. This outperformance by select discretionary names and the concentration of major U.S. indices has led markets to all-time highs while breadth remains quite low. Many companies are struggling and are displaying recession-like attributes. We think this issue is being ignored by many, but we are paying close attention.

Lower and middle-income consumers have been hit hardest by rising costs on daily essentials like groceries and gas. Meanwhile, wealthier investors have benefited from stock market rallies and rising home values. Recent data from JPMorgan’s Cost of Living Survey found that income bracket was a large factor in Americans’ varying views of the current state of the economy.

We think this trend presents a strong opportunity for investors to rotate capital away from high-growth discretionary names to staple names that have been beaten up recently. We have been actively making this rotation for a few months and now own some very high-quality North American staples which we think will relatively outperform over the next few quarters.

High risk sell off

We blinked, and it seems that within weeks, the overall cryptocurrency market will be in a bear market. Bitcoin was down by almost 5% on Tuesday morning and reached its lowest price since mid-April, below $92,000. Bitcoin now has a negative return in 2025 and is down over 14% over the last month. The selloff of Bitcoin could get worse, according to experts, as $93,000 was a key support line, and losses could accelerate below that price point.

Other cryptocurrencies like Ethereum, Solana, and XRP are also having rough months and drawdowns as investors rotate capital away from high-risk assets.

A few factors are currently worrying investors and weighing down risky assets, including Nvidia’s earnings, which were released on Wednesday, September’s nonfarm payrolls report due to be released on Thursday morning, and a BIG monetary policy decision to be made in the U.S. in December by the Federal Reserve. If September’s non-farm payrolls reflect a strengthening job market, it would strengthen the case for the FED not to cut interest rates at December’s meeting.

We would warn investors that now might not be the time to load up on risky assets like crypto, as the trend, at least short-term, points to lower prices.

Massive AI alliance

A day before Nvidia was due to report earnings, the company announced a massive AI partnership alongside Microsoft and Anthropic. According to the companies, the $30 billion partnership will see Nvidia invest $10 billion and Microsoft $5 billion into Anthropic, and Anthropic will purchase $30 billion in computing capacity and 1 gigawatt from Microsoft Azure.

For those of you who do not know, Anthropic is one of the high-flyers in private markets. The AI startup was founded in 2021 and is developing a family of large language models named Claude. The company researches and develops AI to “study their safety properties at the technological frontier” and uses this research to deploy safe models for the public. As of September, the company was valued at $183 billion. The company’s investors include Alphabet, Amazon, and LightSpeed Venture Partners. According to specifics from Nvidia and Microsoft’s investment, Anthropic is now valued at $350 billion.

Under the terms of the agreement, Anthropic will use Microsoft computer capacity as it scales its AI flagship assistant.

According to Nvidia’s CEO, this partnership is a dream come true as he has admired the startup for quite some time. Nvidia will work with Anthropic to support its future growth, and the companies will work together on engineering and design to optimize Anthropic’s models for performance and efficiency.

Microsoft has invested billions into Anthropic competitor OpenAI since 2019 and currently holds a stake that is valued at $135 billion.

This partnership is yet another example of circularity between Nvidia, a hyperscaler, and an AI startup. The circularity continues. The commitments continue to get bigger, and many are fueling sales for the company, making the investment.

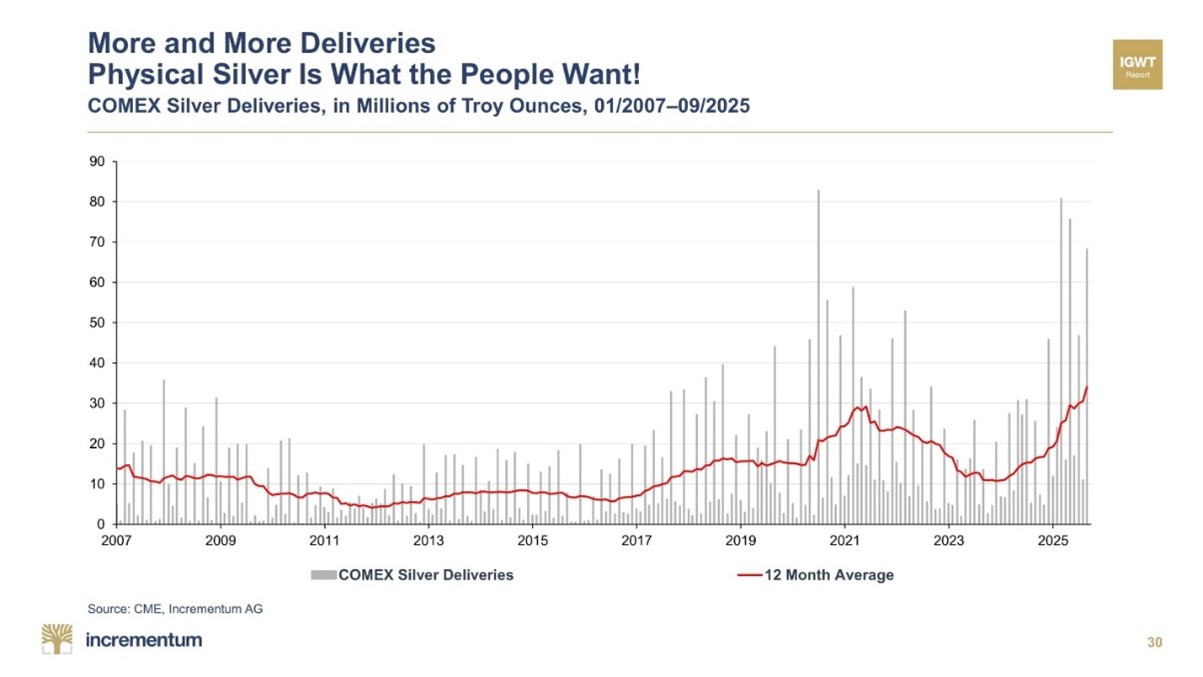

Demand for metals

COMEX continues to report strong silver demand as deliveries spiked once again in September. The commodity exchange delivered nearly 70 million ounces of silver in September, the third-highest monthly total in 5 years:

We have forecasted a silver catch-up as the metal’s price performance has lagged gold in the recent cycle. We think demand will continue to remain elevated, especially as more and more investors seek safety, protection, and diversification.

We continue to evaluate the precious metals trade, including physical silver markets. Silver markets have slightly loosened as manufacturing has slowed. Industrial consumption of Silver is expected to fall by 4% this year; however, demand will not fall enough to reverse the current imbalance in the marketplace. Analysts believe the supply deficit for Silver is still enough to support prices at record highs. While industrial demand has weakened for Silver, investment demand has more than made up for that. Metals Focus, a British research firm, said that inflows into Silver ETFs have increased by 187 million ounces so far this year.

Weakness in physical Silver markets has been offset by gains in key markets including India, Germany, and Australia.

Over the past year, tariff threats from President Donald Trump prompted an unprecedented amount of Silver to flow into New York vaults, creating a shortage of physical metal in London. Growing investment demand and record imports into India quickly depleted all the physical stockpiles in London vaults, causing spot prices to rise sharply compared to CME futures prices. Meanwhile, Silver lease rates recently hit record highs.

Metals Focus Director stated that global consumption would have to fall significantly to rebalance the market and decrease spot prices in a significant manner. They also forecasted the price of Silver to hit $60 an ounce next year, with an average annual price of $57.

We continue to remain bullish on the precious metal and the miners in the industry.

Disclaimer: MacNicol & Associates Asset Management holds shares of mutual funds, ETFs, and stocks that hold or mine Silver.

Left-wing state U-turns

We do not get into politics in terms of giving opinions on policy or ideas. We simply discuss political topics that impact our decisions as an investment manager. After all, elections, policy decisions, and spending Bills are often major drivers of equity markets. It would be a disservice to our investors to ignore all things political.

We bring this up due to a story we read this week. The story lays out New York State’s energy policy, which took a huge U-turn this week. Governor Kathy Hochul halted the implementation of the All-Electric Building Act (a 2023 state law that banned gas in new residential developments).

Hochul cited affordability, technology readiness, and consumer choice concerns as reasons for the reversal. Critics of this Bill voiced the same concerns back in 2023 when the Bill was passed. However, it took reality for Hochul and other politicians to understand the issues that this Bill could cause. This correction was forced by voters and the market. New York went from an all-electric housing plan in 2023 to approving a $1 billion pipeline expansion this year (a long-delayed expansion of an existing pipeline that will bring more Pennsylvania natural gas to Long Island and New York City).

The 2023 Bill was a big win for climate advocates, but it was one that was detached from market fundamentals. This move by Hochul and her recent commitment to nuclear energy are due to a pending election she faces next year. Affordability has become a major focus for voters. Most consumers like the idea of green/clean energy until it impacts them. What we see now is a reversion to the mean, where we see commitment from politicians and investment in nuclear and fossil fuels.

New York’s experience reflects a broader truth for the rest of the nation. High-cost states risk losing investment as industrial electricity demand surges. States that legislate through prohibition and political signaling risk higher costs, slower growth, and eroded credibility. States that pair ambition with realism and invest in renewables, nuclear, and dependable gas supplies will attract capital. Companies want predictability when making an investment in a state; energy transitions take decades; political cycles do not. The mismatch between the two has led New York to its position today and has more than likely deterred certain firms from investing in the state, especially companies that are building out data centers.

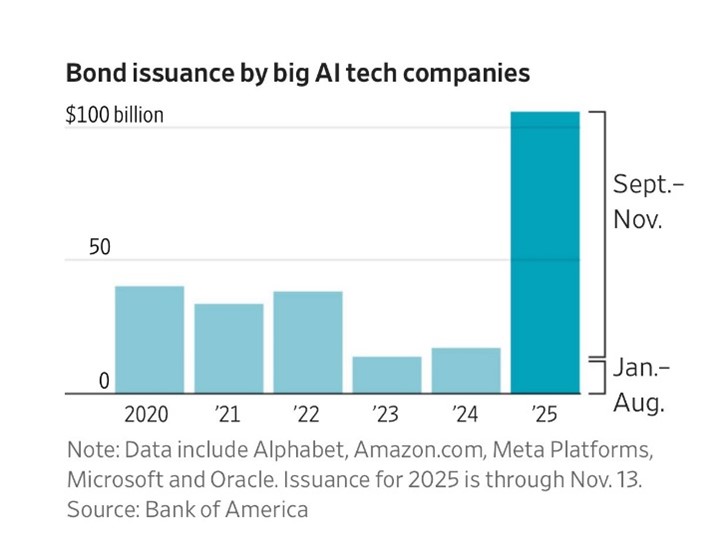

A chart that explains leverage in AI

Last week, we talked about the growing worry from certain investors regarding leverage in the AI industry. Numerous firms have piled on leverage to increase capex in AI. We mentioned that CoreWeave doubled its debt in a matter of a few months, and the issues Meta and Oracle could face due to their added leverage moving forward. This week, Bank of America released a study that looks at bond issuance by big AI technology firms. The graphic below tracks bond issuance from five of the largest hyperscalers.

Bond issuance has surged since September at the top of the technology industry as hyperscalers look to finance massive data centers. The value of private construction on data centers has surged in the last 5 years, increasing from below $10 billion to over $40 billion. According to Morgan Stanley research an estimated $2.9 trillion is expected to be spent between 2025 and 2028 in order to finance data centers. The data center spending will come from a variety of sources, including private credit, private equity, corporate bonds, and technology company spending. Technology companies simply will not generate the cash flows to finance these projects; they will look to debt and equity markets for the first time in years to finance their large endeavors.

Numerous firms have warned investors and tech firms about this strategy, as it comes with major risks. At the same time, there is elevated investor appetite due to AI growth prospects and the fear of missing out.

Oracle is by far the most indebted tech giant in the mix; the company is angling to be the go-to computing provider for labs like OpenAI and will need to borrow billions more to finance its endeavors. The company does not generate nearly enough cash flows to finance its projects. Oracle’s credit rating is reportedly deteriorating according to S&P and Moody’s, who are edging closer to reclassifying Oracle bonds as junk debt. Oracle shares are down 30% over the last few weeks; their bonds are down 7%.

There is also a risk of obsolescence for tech firms leveraging themselves to spend on capex and chips in just a few years. Technology has always improved efficiencies across industries, but the level of capex spending on data centers and the power required to power them is nowhere near efficient. We think something will eventually give.

The last time Wall Street and investors went all in on an industry was the fracking boom, which was followed by a bust over a decade ago. This time, the financing is even larger and more widespread. Pay attention.

MacNicol & Associates Asset Management

November 21st, 2025

Download in PDF format: