Share This Post Today!

Recalada a Bahía Blanca Light, Monte Hermoso, Argentina

This lighthouse was built in 1906 and is the tallest lighthouse in the southern hemisphere standing at 220 feet tall. The lighthouse station is staffed and is open to guided tours.

Delimara Lighthouse, Marsaxlokk, Malta

This active lighthouse was originally constructed in the 1850s. The original structure seen in this photo was replaced by a modern structure in the 1990s. However, the original base of the structure remains. The lighthouse is located on Maalta’s coast and has a nautical range of 18 miles.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Micron’s big announcement

On Saturday, it was reported that Micron Technology plans to acquire a chip-making facility in Taiwan. The acquisition will help Micron boost manufacturing capacity. Micron reportedly will pay $1.8 billion as the U.S. memory chip company attempts to keep pace with the industry in terms of manufacturing capacity amid growing demand across the sector. Micron is acquiring a manufacturing facility from Powerchip Semiconductor Manufacturing Corp. This transaction will add about 300,000 square feet of cleanroom space; a heavily controlled environment needed for chip production. Micron has key production facilities in Taichung, Taiwan, for its product line.

Memory chips are a vital component of AI accelerators and are necessary for processors like Nvidia’s product. The need for memory components in AI hardware has increased costs substantially. Memory prices surged between 40% and 50% in the final quarter of 2025 and are expected to increase at a similar rate in the to start 2026, according to Counterpoint Research.

Micron’s biggest rivals include Samsung and SK Hynix in making HBM chips. Both firms have invested heavily in increasing production capacity. SK Hynix recently announced plans that will see the South Korean firm invest $13 billion into building a processor-packaging plant. Micron is also a leader in the market for dynamic random-access memory, which is used on desktop computers and servers.

Just last week, Micron broke ground on a New York-based chip-making complex that the firm says will eventually be a $100 billion facility.

Micron shares have been on a tear this year and have more than tripled over the last year. The firm has been operating in Taiwan for more than 30 years and is the country’s largest foreign investor.

The deal is expected to close by the second quarter of 2026, subject to regulatory approvals.

Trump’s threats heat up

2026 has already been quite the year for the Trump administration. They have arrested former Venezuelan President Maduro, they are investigating the Federal Reserve Chairman for white-collar crimes, they are inquiring into the purchase of Greenland from Denmark, and they are even introducing new tariffs. Quite the roller coaster just three weeks into the new year.

On Tuesday, stocks moved lower, and yields moved higher due to recent Trump threats, which could upend global trade. Trump is now threatening higher tariffs on European NATO allies if a deal for the U.S. to purchase Greenland is not reached. According to Trump, eight European countries will face increasing tariffs starting at 10% on February 1st to 25% on June 1st if a deal is not reached.

The European nations that will face these tariffs are considering retaliating against U.S. exports, and some experts expect the entire European Union to activate its anti-coercion tool (first developed in 2023 in response to Chinese pressure on Lithuania). This tool is described as a nuclear option for trade and has a high bar to activate. Half the countries of the EU would have to sign off, which right now seems unlikely due to the EU’s reliance on the U.S. for security, supplies of natural gas, and a strong export market. We expect the first move from the EU to be against technology companies if tensions continue to escalate. The EU could place restrictions on the European operations of Netflix or U.S. cloud providers. This could further accelerate; the EU could eventually ban U.S. companies from public procurement or suspend profit rights in Ireland for U.S. firms.

The industries that could be most affected by a European retaliation on the U.S. include aircraft, cars, agriculture, and bourbon. European Commission head Ursula von der Leyen has reiterated that Greenland’s sovereignty is non-negotiable. Greenland has repeatedly said it is not open to being a part of the U.S. However, the U.S. is reportedly going to make a large offer that they want the people of Greenland to consider and vote on.

Secretary Scott Bessent warned European leaders against retaliatory tariffs at the World Economic Forum this week. He pointed to China’s retaliations in April 2025, which led to even stiffer tariffs for the Chinese.

Currently, the U.S. only has a military presence in Greenland. The Danes have indicated in the past that they are open to an even larger footprint from the U.S. in Greenland.

It really seems like Trump and his allies are focused on securing the Arctic. He has stated that Greenland is critical for U.S. security. Greenland would give the U.S. a major presence in the Arctic. Greenland would also provide the U.S. with a place to set up anti-missile defenses to intercept action from Russia and China.

We are not saying that any of the above will occur, but we still believe this will be solved diplomatically. However, it is a major risk factor that is impacting financial markets. On Tuesday, markets moved lower on this news as investors began to worry about new tariffs and a potential new conflict. Tech, AI, and high-growth stocks were amongst the groups that were hit the hardest. Gold, oil, and consumer staples moved higher as investors continue their rotation into stable and defensive assets.

Source: Finviz

After a few negative days for financial markets, President Trump stated that the U.S. will not utilize force to take Greenland in a speech at the World Economic Forum. Trump said the U.S. would be “unstoppable” if he chose to use the military, but that he would not go that far. Trump went on to say that the U.S. would be able to fully defend Greenland with full ownership. He also stated that the U.S. needs Greenland to complete its golden dome.

Regardless of how you feel about Trump, Wednesday’s tone was positive for the world, financial markets, and Greenland.

Netflix earnings

On Tuesday, Netflix released its most recent quarterly earnings, and the results were quite mixed in our opinion. The company beat adjusted earnings and revenue estimates by small margins.

Netflix reported EPS of $0.56 (vs. $0.55 estimated), and revenue of $12.05 billion (vs. $11.97 billion estimated).

However, their guidance was softer than expected. Netflix is predicting an operating margin of 31.5% for 2026, 110 basis points lower than analysts had expected. Netflix stated that this figure is lower due to expenses related to their pending acquisition of Warner Bros Discovery. The deal will add $275 million in costs this year on top of $60 million spent in 2025 on the deal. The company also expects to increase spending on content by 10% in 2026, which will weigh on profit and margins.

The streaming giant also announced that it had revised its offer for Warner Bros Discovery to an all-cash deal, valuing assets at $27.75/share. The all-cash offer aims to provide certainty to Warner Bros shareholders and accelerate a shareholder vote by April. Netflix is not the only company making a bid for Warner Bros. Paramount, Skydance made a hostile bid for Warner Bros last year, and their all-cash offer sits at $30/share. Warner Bros. leadership has backed Netflix’s deal. Paramount’s pending offer expired on Wednesday at 5pm (unless otherwise extended).

The deal is worrying some investors as Paramount could trigger a bidding war. This pending deal from Netflix completely differs from its historic growth strategy of build, don’t buy. It’s no surprise that shares have lost more than 10% since the deal was announced.

We expect any kind of deal that involves Warner Bros Discovery to face heavy regulatory scrutiny, as a high-profile acquisition like this one could monopolize the market.

Netflix’s co-CEOs discussed the competitiveness in the entertainment and streaming industries on their earnings call. Management will reportedly be looking to improve the variety and quality of series and films on their platform this year due to the heightened competitiveness across the industry. Gary Peters, one of the co-CEOs, tried to dappen the lower-than-expected guidance, stating that previous internal targets were only “long-term aspirations” and not an actual forecast. He also stated that their goals were based on organic growth and did not include the impact of M&A.

After amending their deal to an all-cash offer, Netflix made an announcement that surprised many investors: they are pausing their share buybacks in order to fund an eventual Warner Bros deal.

On the positive front, Netflix surpassed 325 million paid subscribers last quarter and expects its advertising revenue to more than double in 2026. Netflix’s subscriber count grew by 8% last year. The company went on to say that its priorities for this year will be to continue building out its live sports programming, expanding its podcast platform, and closing the Warner deal.

Despite reporting growth and some strong numbers and changing their Warner offer to an all-cash deal, Netflix shares moved lower on Wednesday morning. Ten Wall Street analysts covering Netflix also cut their price targets following the streaming giant’s earnings report. It seems investors and analysts put more weight on Netflix’s weaker guidance and the pause of share buybacks.

We think the recent pressure that Netflix shares have been under could continue for a variety of reasons. However, if this deal is carried out properly and Netflix continues to grow its advertising revenue and subscribers, it will continue to be poised for long-term growth. We will warn our readers that long-term growth does not always equate to higher stock prices. Other factors matter, including valuations. In terms of Netflix valuation, we think the company’s share price is high on an absolute basis but is on the cheaper end of its historical average valuation. The valuation of Netflix has compressed in recent years as the company matures, its subscriber growth slows, and the competitiveness of the entertainment industry increases.

The realities of nuclear energy

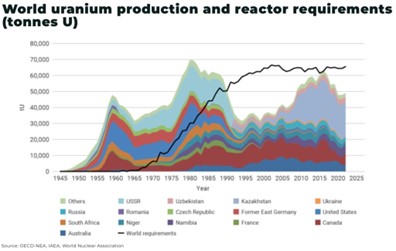

For years, we have discussed nuclear energy, uranium supply and demand, and opportunities to profit in equity markets from these trends. For long-time readers, you know we have exposure to miners, physical uranium, and ETFs that hold uranium miners, producers, or companies involved in uranium enrichment. It has been a long-term trade that we believe will pay off for a variety of reasons. We think uranium prices will move higher, which will push equity prices higher across the sector.

Global uranium demand continues to increase as countries and companies push their green agendas. Many countries have reclassified nuclear energy as a renewable energy source due to the realities of scaling solar, wind, and hydro energy. Government and companies across the world are investing heavily in the sector to secure reliable energy supplies, address their increased energy demand, and decrease their reliance on fossil fuels. On top of that, 14 major financial institutions, including Goldman Sachs and Bank of America, have pledged support to triple global nuclear energy capacity by 2050. More than 120 companies headquartered across 25 countries have also signed the pledge.

Last year, global uranium demand increased to a record high as the nuclear renaissance continues:

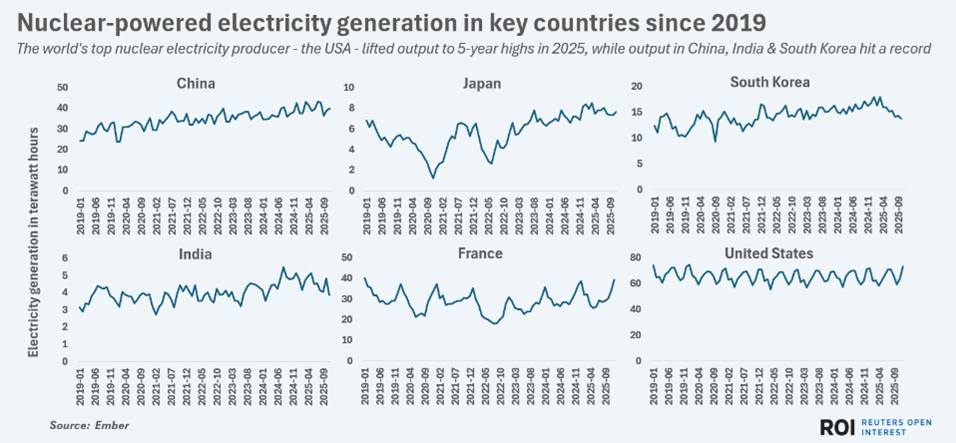

Demand is expected to continue to accelerate as the grid rotates further toward nuclear energy, and technology firms expand their electricity consumption due to AI data centers. Governments around the world are supporting this increased demand through heavy investment and expediting approvals for nuclear energy projects. Countries around the world are rushing to compete and develop nuclear power generation projects to address the growing demand. Nuclear power generation in numerous key countries hit multi-year highs last year.

The Trump government has followed the lead of the French government when it comes to nuclear energy over the last year, as they have committed billions to the industry, announced the reopening of old nuclear reactors, expedited approvals for new reactors, bolstered domestic production, and integrated nuclear power into national security. The French have long been advocates for nuclear energy usage and were the first developed nation to classify nuclear energy as a renewable energy source. As of Q2 2025, 439 reactors are operating globally, with another 62 under construction and 110 in the development phase.

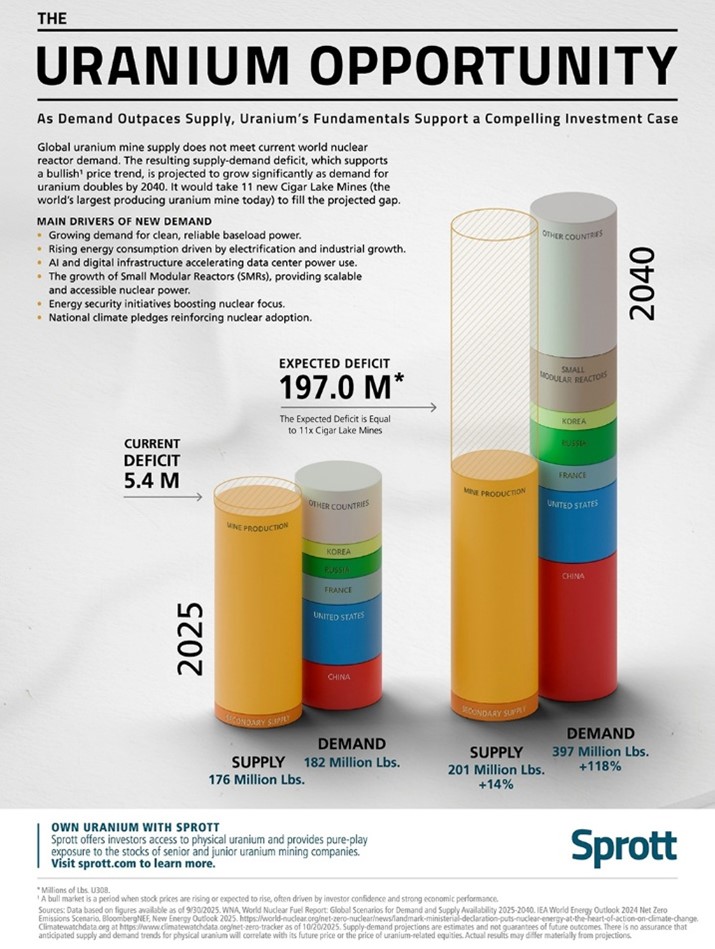

Here is a graphical illustration from Sprott that illustrates the supply and demand of uranium today and what it will look like in 15 years:

Talk about an opportunity and a supply deficit. As more uranium mines come online across the world, many forecast that the largest uranium producer, Kazakhstan, is in the midst of peaking and has already begun to limit volume. Currently, Kazakhstan produces 40% of the world’s uranium. Kazakhstan addressed the increase in global demand in the 200s by ramping up production from 2.1 tons in 2001 to 24.6 tons in 2016. A 10x increase in 15 years helped address growing demand. This time, there is no Kazakhstan coming online as mines continue to deplete. On top of that, new supply takes years to bring new production online (according to the Oregon Group, it can take up to 13 years from discovery to production for uranium mines).

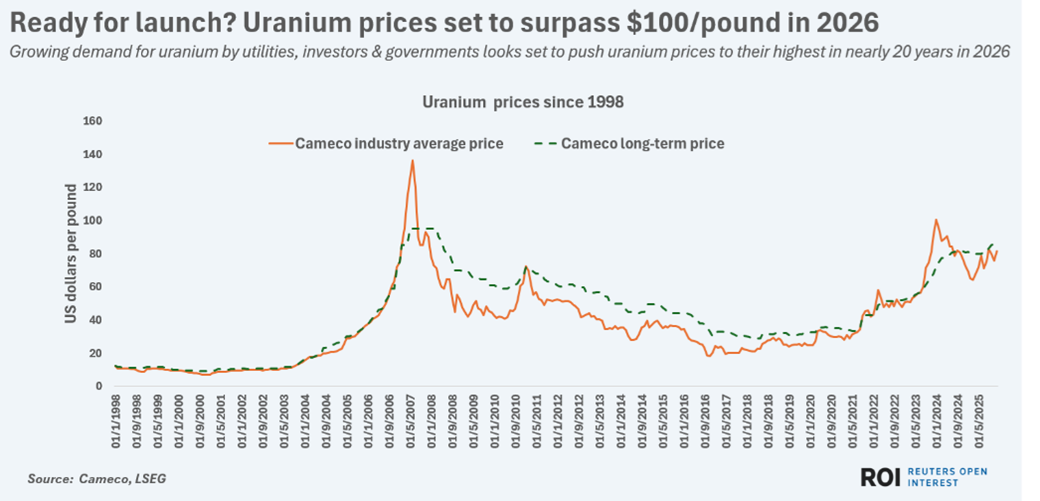

Physical uranium prices increased by 11% last year, according to Cameco. That rise was much lower than the performance of most uranium-based equities, which saw their stock prices increase by more than 100%. This increase was justified by supportive government legislation, increased demand forecasts (due to the AI-fueled boom), and shrinking global production. Many of the beneficiaries of this trade are looking to ramp up production over the next few years.

U.S. production is expected to hit 1 million pounds this year, compared to U.S. consumption, which is expected to be 50 times higher. This supply-demand mismatch is, in turn, causing upward pressure on U.S. uranium prices, which is forecasted to intensify in 2026.

Cameco is forecasting the price of uranium to surpass $100/pound this year:

While spot prices remain below $90/pound, executives tracking conversations between uranium suppliers and power generators have noted long-term pricing contracts are near $100/ton. If these deals are confirmed, fresh momentum could spark in the spot market.

The combination of lower stockpiles in the U.S. and restrictions on imports (Russian uranium) has placed more focus on the spot market as demand increases. Purchases of uranium by investors have also tightened supply in the U.S. market. Uranium holdings by Sprott’s investment vehicle (SPUT) increased by 9 million pounds last year and hold 72.5 million pounds of physical uranium (versus 40 million in December 2021).

We expect that as the global nuclear reactor fleet increases and operations begin, investor holdings of uranium will continue to grow, which will further add momentum to prices.

Companies like Cameco will benefit greatly from higher prices, but many small-cap names offer more torque with exploration upside and M&A potential. Most of the largest uranium-producing companies are located in Kazakhstan, Russia, and China. There is great potential for North American players as they ramp up production and begin to eventually compete with Cameco.

We think a diversified approach is the best way to manage risk and reward in the uranium trade. Our investment focus remains in North America through a variety of equity securities, including exposure through stock, ETFs, and trust units of vehicles that hold physical uranium.

Disclaimer: MacNicol & Associates have equity exposure to the nuclear industry through uranium mining companies and ETFs that hold uranium miners. We also have exposure to physical uranium through a TSX listed investment vehicle.

What we are looking at next week

Markets whipsawed this week after Donald Trump threatened to impose tariffs on Europe tied to renewed demands around the acquisition of Greenland. While he later played down his tone in a speech at Davos (World Economic Forum), the initial rhetoric revived fears of a transatlantic trade conflict and reintroduced geopolitical risk into what had been a relatively stable macro backdrop. Equities weakened, the dollar came under pressure, and investors rotated toward defensive positioning as confidence in the near-term policy environment deteriorated.

Against that backdrop, attention next week turns squarely to the Federal Open Market Committee (FOMC) meeting on Wednesday. This will be the first FOMC decision since markets were confronted with a combination of tariff threats, political pressure, and questions around policy credibility. We do not expect a rate cut; the focus will be on tone, forward guidance, and the extent to which the Fed reinforces its independence and data-driven framework. In a fragile market, language matters more than the decision itself, and given the recent ramp-up in rhetoric, we will be listening closely.

The broader question heading into next week is whether policymakers can help stabilize expectations after a confidence shock, or whether recent weakness marks the beginning of a more persistent repricing of risk, as it did at the start of last year when Trump similarly went on a tariff campaign. A firm and disciplined message could help contain volatility, while ambiguity risks validating the emerging “sell U.S.” narrative. As we look ahead, investors should be focused less on short-term market moves and more on how policy credibility and geopolitical risk are shaping the environment going forward.

MacNicol & Associates Asset Management

January 23rd, 2026

Download in PDF format: