Share This Post Today!

Palagruža Lighthouse, Palagruža, Croatia

This lighthouse is located on an uninhabited island in the Adriatic Sea. The island can only be reached by chartered motorboat. The journey takes several hours from nearby islands.

Pokonji Dol, Croatia

Pokonji Dol is an islet in the Croatian part of the Adriatic Sea, which is situated 500 meters south from Hvar. The lighthouse built on the islet was built in 1872. The lighthouse ensures safe navigation of vessels coming from the open sea.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

First comes energy, then comes?

When the conflict in Iran began a few weeks ago, a lot happened, markets have become even more unstable, energy prices have surged (oil prices remain well above $100 per barrel as of this writing despite Trump pushing for an end to the conflict and pushing for the Strait of Hormuz to be reopened), and global trade through the Strait of Hormuz has crawled to a stand still (reportedly, (there are many reports that the Chinese and Iranians continue to transport cargo including oil through the area)). Many investors have added energy names to hedge against higher energy prices and or benefit from their underlying stock price increases. We believe the price of oil and many other energy commodities will remain elevated for some time, as uncertainty persists in the global geopolitical landscape.

Rising energy prices from this conflict will be felt across the economy, and consumers will feel it beyond the gas station or when they pay their energy bills. At the pump, prices have surged to $4 a gallon, the highest since 2022 (increasing 30% over the last month, according to Barron’s). Higher energy prices will ripple across global supply chains and have many second-order effects on industries, including the food and chemical industries. Both sectors are heavily dependent on natural gas and petroleum-based inputs for everything from fertilizer and packaging to transportation and industrial feedstocks. As a result, cost pressures that began in crude and gas markets are now migrating downstream, leading to higher realized and expected prices in food commodities and chemical products. That is a problem for the global economy.

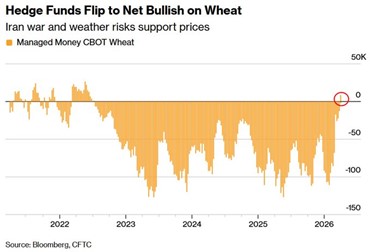

The current conflict in Iran, paired with a poor weather forecast for this harvesting season, has led hedge funds to turn bullish on the price of wheat for the first time since June 2022. The Strait of Hormuz being closed has not only halted crude and natural gas exports from the Middle East, but it has also impacted fertilizer flows worldwide. According to the World Economic Forum, the Arabian Gulf accounts for at least 20% of all seaborne fertilizer exports. The dependency is even more acute for urea, the world’s most widely used nitrogen fertilizer, with 46% of global trade originating from the region.

This disruption will impact global food security and will benefit many fertilizer producers’ underlying earnings and margins. The few public firms on Western exchanges have already seen a nice bump in their stock price since this conflict began. A prolonged conflict and supply disruptions will also possibly lead to many producers switching the crops they grow to crops that require fewer nutrients as the supply of fertilizer shrinks. According to market experts, consumers in the African and European regions are already feeling these price increases. UBS even warned its clients this week that the food price shock could hit even harder than the energy spike. Their argument boils down to energy as an input in food production, transportation, and refrigeration.

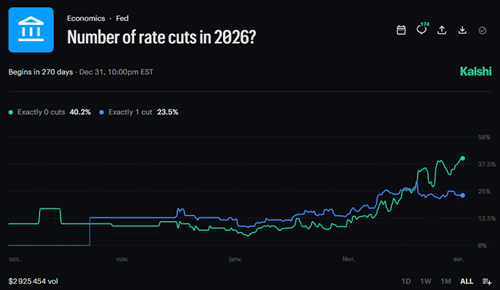

Higher food prices will add even more inflationary pressure to the global economy. Do not be surprised to see the consumer price index of many countries moving higher in the coming months. Food inflation is one of the stickiest portions of the CPI and could completely alter the Fed’s path forward. These major warnings have led some market experts to point toward potential stagflation, a market where there is stagnant growth but high inflation (a double negative for investors and consumers). According to the odds platform, Kalshi, the probability for 0 rate cuts by the FED this year is higher than 1 rate cut, quite the change in odds over just a few weeks.

We will say all of the above was written before Tuesday evening’s big announcement.

Tuesday night pause

On Tuesday night, at the eleventh hour, both Iran and the U.S. announced a two-week ceasefire. This ceasefire came after massive threats from the Trump administration against Iran. Ironically, both sides in this conflict claimed short-term victory after it was announced. Trump announced the U.S. will stop bombing Iran, and Iran stated it will not attack their adversaries and will reopen the Strait of Hormuz if the vessel coordinates with the Iranian military. Numerous countries across the world, including Saudi Arabia, backed the ceasefire.

The ceasefire announcement led to a surge in future prices of equities and precious metals. The price of oil collapsed by more than 15% on Wednesday morning, where it was trading in the mid $90 range. Yields also pulled back across the world as traders priced in a higher probability of less inflation risk (stemming from a prolonged conflict).

Investors welcomed this news with open arms despite the deal being temporary, as global commerce has screeched to a halt and energy prices have surged. According to Bloomberg, as of Tuesday, there were more than 800 vessels still trapped in the Strait. Expect the log jam to unwind in the next two weeks. Flows through the Strait ticked up in the days ahead of Trump’s Tuesday deadline, but remain 90% down on normal levels. According to Kpler, of the 800+ vessels stuck in the Persian Gulf, 426 are carrying oil, fuel, and gas.

We will say that the markets’ reaction on Wednesday morning might be an overreaction as the ceasefire is very temporary and both sides remain far apart, and the Iranian’s will still control the Strait of Hormuz very tightly. MarketWatch compared Iran’s oversight of the waterway to a strict Iranian toll booth. We would not bet on lower energy prices in the short term, even with this joint announcement by the two sides. There is still a great risk that energy prices move higher or remain elevated for quite some time.

On Wednesday, unsurprisingly, energy, chemical, and fertilizer stocks all pulled back heavily. Some of these moves present strong buying opportunities in our opinion, as supply disruption risk remains in the market, which could reverse Wednesday’s trend quite quickly. For the most part, we have not gained any large exposure in the chemicals sector as chemical stock prices began to run at the initiation of this conflict and, in our opinion, were extremely overbought. This made us avoid them over the last month. We still like many of the energy names we hold, even without this conflict, as they are attractive from a fundamental standpoint. We had been slowly increasing our energy exposure at the end of last year due to uncertainty in geopolitics and the low multiples many companies were trading at.

Oil prices bounced slowly on Wednesday after the Secretary of Defense stated that the U.S. would still be hanging around in the region, stating, “we’re not going anywhere”.

Dimon’s letter

Jamie Dimon released his annual letter to shareholders. We are not going to bore our readers with details regarding JPMorgan Chase’s operations and earnings. We want to highlight something that goes beyond the bank and that will have ripple effects across the global economy. Dimon warned investors that private credit losses will be larger than many fear. This comes seven months after Dimon stated, “When you see one cockroach, there are probably more”. The statement was in regard to bad loans in the private credit space.

Dimon stating that losses will be greater than expected heightens his previous statements on private credit. JPMorgan has been lightening its exposure to the asset class over the last year. Dimon stated that looser credit conditions will lead to higher-than-expected loan losses and potential delayed payments from borrowers.

Despite this bearishness and private credit warning, Dimon did state that the “U.S. economy remains resilient with consumers still spending and earning” despite “an unsettling landscape”. Dimon went on to say that there are a few economic tailwinds that will assist the U.S. economy, including the FED’s bond buying program, and the White House’s agenda, which includes deregulation and the Big Beautiful Bill. He did go on to say that the world and consumers will have to deal with an energy shock that will have many ripples stemming from the new conflict between Iran and Israel.

Overall, Dimon’s comments were not shocking; however, his private credit warnings were amplified when compared to last year. If these issues in private credit persist, many investors, including institutions, could face some serious issues. It seems the smart money is attempting to minimize exposure and avoid the space right now, as there could be some serious skeletons in the closet.

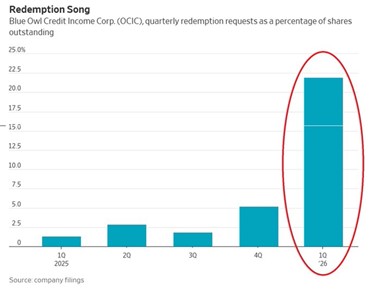

Speaking of the issues in private credit, according to filings this week, Blue Owl’s credit income fund reported more than 20% in redemption requests (as a percentage of shares outstanding). Blue Owl caps redemptions at 5% per quarter, so investors are receiving less than a quarter of the money requested.

Investors cannot access their capital, and many worry valuations do not reflect what holdings can actually be sold for, which could lead to some serious write-downs or NAV decreases in these funds.

It is becoming a weekly tradition for us to report on the latest issues in private credit. What started as a small problem has ballooned and become a real problem for financial markets.

Delta earnings

Delta reported its quarterly earnings on Wednesday morning ahead of the market open; the earnings, paired with the fresh ceasefire announcement, proved to be strong tailwinds for shares as they jumped by more than 10% in pre-market trading.

Jumping into the earnings, Delta reported $1 billion in pretax profit despite a quarterly increase in fuel costs of $2 billion. Delta beat quarterly earnings and revenue estimates despite realizing higher fuel costs during the quarter, uncertainty continuing to remain present across the global economy, and as consumers’ balance sheets continue to deteriorate. Most U.S. airlines have not engaged in any hedging activities in terms of fuel costs since 2010, so higher prices often directly hit company income statements. Management stated that demand remains strong and expects profit for the quarter ended in June to land at $1 billion.

Delta stated that it will be cutting capacity to mitigate an increase in the price of fuel. Higher prices also slightly benefit Delta as the airline owns an oil refinery, which, according to their second quarter guidance, will benefit the company “to the tune of $300 million”. Delta is the only American airline to own an oil refiner.

Delta earnings, along with those of other airliners, will be very tough to predict through this year due to the uncertainty surrounding the Iran-U.S. conflict. According to Barron’s analysts, ’ earnings-per-share for Delta for fiscal 2026 range widely from $0.15 to $7.50, reflecting the instability of fuel prices.

Overall, Delta’s earnings were fundamentally solid. The company’s revenue mix shifted further toward higher margin segments in the quarter. The company’s balance sheet and cash generation continued to strengthen this quarter.

Delta’s competitors also enjoyed a nice bump in their share price on Wednesday morning as the company’s strong report (coming at a time of great uncertainty and higher costs), paired with a ceasefire, got investors much more bullish on the sector and markets as a whole.

We do not hold any major airline stocks but follow the majors closely as their earnings give many insights into the health of consumers’ finances. During this quarter, airline earnings will give us valuable insights into the health of the economy as the industry sits at the intersection of consumer demand, energy markets, and global commerce – making the sector a great gauge of economic momentum and confidence.

Carry trade blowing up

As we’ve discussed periodically in our newsletters over the past two years, the Japanese carry trade has blown up and is changing how investors approach markets. For those new here, the Yen carry trade involved investors borrowing in Yen (at close to 0% interest rates) and purchasing assets in other currencies that yielded much more (U.S. stocks, fixed income).

The Japanese 30-year bond is now yielding 3.58% (orange line) according to FactSet:

Source: FactSet, Japan 10- and 30-year yields

In 2020 and 2021, the 30-year rate was well below 1%. The increase in rates since then has blown up the carry trade. Yields for the 30-year bond in Japan are trading near all-time highs (the bond was introduced in 1999). Japanese yields fell on Wednesday after the ceasefire between Iran and the U.S. was announced, as inflation fears had pushed yields much higher over the last few weeks.

For the first time in decades, Japan is dealing with major inflation fears at a time when its Central Bank is actively reducing its holdings of bonds, and its parliament passed a record spending package. Bond investors are simply demanding higher compensation for holding Japanese securities, and the Bank of Japan is no longer stepping in to suppress yields.

We think we are in the midst of a major structural shift in how Japan is priced globally. This matters for not just bonds, but also for equities, bank stocks, the Yen, and capital flows.

What we are looking at next week

Investors heading into next week will be focused on whether the recently announced truce for the war in Iran holds, or if it proves to be a temporary pause in a still-fragile geopolitical backdrop. The market’s initial response has been constructive, but there remains a clear hesitation beneath the surface, as participants assess whether risk assets can sustainably recover without a definitive resolution. Recent volatility tied to the conflict in Iran has already left a mark on sentiment, with positioning reflecting a more cautious tone than headline index levels might suggest. In this context, the durability of the truce is not just a geopolitical question, but a key determinant of whether confidence can rebuild in a meaningful way. We live in a time when things can change on a whim, and that is typically not a backdrop that builds confidence in investors.

At the same time, the economic implications of the conflict continue to linger, particularly through elevated energy prices that have yet to meaningfully retrace. While crude oil did see its largest one day drop in years, prices are still around 50% above where they were mere weeks ago. Even with a ceasefire in place, the structural tightness in energy markets remains, and this feeds directly into inflation expectations and broader macro uncertainty. Investors will be watching closely to see whether markets can look through these pressures and reprice toward a more optimistic growth outlook, or if higher input costs begin to weigh more heavily on forward expectations. This creates a tension between geopolitical relief and economic reality, which will likely define trading conditions in the near term. Ultimately, next week’s tone will be set by whether stability persists long enough for markets to regain conviction, or whether underlying fragilities reassert themselves.

April 10, 2026

MacNicol & Associates Asset Management

Download in PDF format: