Share This Post Today!

Castle Point Lighthouse, Castle Point, North Island, New Zealand

This lighthouse is the North Island’s tallest lighthouse standing 52 metres above sea level and is one of only two left in New Zealand still lit by the original rotating fresnel lens.

Cape Spartel Lighthouse, Tangier, Morocco from Naima E.

The Cape Spartel Lighthouse is located at the cape of the same name, approximately 14 kilometers west of Tangier. This site marks the point where the Mediterranean and Atlantic waters meet. It is one of the largest lighthouses in Africa, marking the southern entrance to the Strait of Gibraltar on the Atlantic side.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Alt managers get some help

In recent months, major issues have been revealed across the private credit industry. Funds throwing up gates, investors redeeming capital in droves, and increases in loan losses. We have been talking about the topic for months now. We bring this up yet again due to an article we read over the weekend. A Bloomberg opinion piece stated that the issues in private credit are overblown.

The article goes all out in protecting private credit. The article acknowledges the risks in the private credit market but claims the losses will be more easily absorbed. We disagree. The mega funds are extremely levered, aligned with private equity funds, and not marking to market their assets. Expect more loan losses, write-downs, and poor returns for investors as many of these funds begin to unwind.

This article was published at a time when first-quarter earnings are being released, as investors look for guidance on the issues in private credit, and to see who is exposed to what. Last week, Wall Street banks released their earnings and, for the most part, had decreased their private credit exposure, looking to be in good shape. On the other hand, alternative managers like Blue Owl, Blackstone, and Ares have elevated exposure and cannot pay out investor redemptions. On top of that, banks are reducing exposure and raising borrowing rates for private credit lending. This could lead to more dominoes falling:

We are watching the figures and headlines very closely, as eventually these private asset managers could be attractive buys in public markets. We also want to make sure we stay ahead of the issues and avoid the junk for our investors. As private market investors, we also want to stay on top of investor flows and liquidity issues, as eventually some secondary opportunities could present themselves. One of the hottest private market asset classes right now is private equity secondaries, which is seeing large inflows. Global secondary volume hit a record US$103 billion in H1 2025, driven by liquidity needs, strong capital availability, and narrowing bid-ask spreads. That matters because the same forces that push investors toward secondaries — slower distributions, tighter exits, and portfolio rebalancing — are often early signals of stress and opportunity in adjacent private-market segments, including private credit. In that sense, secondaries are not just a separate pocket of strength; they may be the early barometer for where liquidity stress — and opportunity — emerges next across private markets.

Traffic picks up

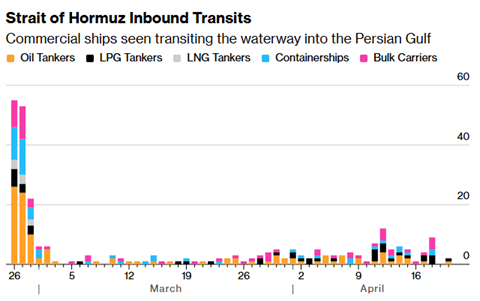

After several weeks of close to no shipping traffic through the Strait of Hormuz, activity began to pick up in the area last week as countries around the world pushed the U.S. to end its blockade of Iranian ports and Iran to end its iron grip on transit in the region. However, just a few days later, traffic has once again ground to a standstill.

Iranian and U.S. officials both claimed traffic picked up in the area last week, leading to a rush of vessels into the area and a sharp decrease in global energy prices. Data suggested this was true; vessel activity was at its highest point in the Strait since the conflict began. However, Iran’s leadership changed course over the weekend, restricting vessel traffic. This move revived fear over global energy supply disruptions, causing prices to move off their lows on Monday morning. On Tuesday, many vessels began avoiding the Strait entirely due to blockages from both Iran and the U.S. The move highlights the markets’ current thinking—a peace deal is in progress but unlikely to happen immediately. As of Tuesday morning, prices continued their rise as it was reported that Iranian officials were undecided on their attendance in Pakistan for peace talks. The current ceasefire ends on Wednesday, and Trump has threatened military action if no deal is agreed to by Wednesday. On Wednesday, Trump announced an extension to the ceasefire, which sent markets higher. Never forget, one of Trump’s barometers of success is the stock market; he hates volatility and uncertainty. Despite the ceasefire extension, energy prices moved higher on Wednesday after Iran’s Islamic Revolutionary Guard Corps said it seized two ships in the Strait of Hormuz.

We are not sure what will happen as the situation is littered with uncertainty and opaqueness. It seems every party involved, including intermediaries, has a separate view on the conflict, which is all being reported in the media. We continue to believe this conflict will not be resolved quickly, but likely at this stage will not accelerate. The one thing that is becoming clearer is that this conflict could begin to spill over into geopolitics across the world. China’s leadership is reportedly very displeased with the blockage in the Strait, which it says is impacting regional and international commerce. If a peace deal is not agreed upon, China will reportedly delay its May summit with the U.S.

Haliburton reports

Haliburton Company, a multinational American energy firm, reported strong first-quarter earnings on Tuesday. The oil servicing company beat revenue and earnings-per-share estimates. Management highlighted the beginning of a recovery in North America and the conflict in the Middle East, which slightly disrupted business. However, Haliburton’s headline numbers were not greatly impacted this quarter due to strong figures from Latin America and Europe, where demand improved during the quarter and offset the slowdown in the Middle East.

Haliburton’s results kick off the results for the global oilfield service providers.

Since the conflict began in Iran, attacks on energy infrastructure in countries such as Qatar and Saudi Arabia have dragged down crude oil production across the region.

Haliburton’s drilling and revaluation, and completion and production business units beat revenue estimates. Free cash flow came in stronger than expected, driven by lower capex. The company’s strong quarter allowed it to return close to $250 million in cash to shareholders through a combination of dividends and share repurchases. On its earnings call, management stated that they expect share repurchases to accelerate through this year.

Haliburton’s CEO stated that he was very pleased with the company’s performance this quarter and went on to say that the company’s continued focus on returns and capital discipline will drive long-term returns for shareholders. Haliburton expects revenue growth in the mid-to-high single digits for the full year, led by Latin America.

After Haliburton reported earnings, shares moved up by 4%.

Disclaimer: MacNicol & Associates Asset Management holds shares of Haliburton Co. across various client accounts.

Warsh has his day in Washington

Kevin Warsh, the FED Chair nominee, had his nomination hearing on Tuesday in the Senate. Investors expected Warsh to face staunch opposition from Democrats after Trump had begun to politicize the FED in recent years, led by his major criticisms of current FED Chair Jerome Powell.

The hearing began as expected, with Republicans for the most part putting their weight behind Warsh and criticizing recent FED actions under Jerome Powell. On the other hand, Democrats labeled Warsh as a puppet for Trump and criticized his personal wealth and dealings with Wall Street firms. Senator Elizabeth Warren stated that Warsh will juice the economy in the short term for President Trump. She also stated that Warsh has more than $100 million in undisclosed assets. Warsh stated that if he were confirmed, he would sell all his assets and convert his wealth into “something like cash”.

Warsh is a Harvard Law School grad who served as a member of the FED Board of Governors from 2006 to 2011. Previous to his experience at the FED, he worked at Morgan Stanley and the National Economic Council. Since his time at the FED, Warsh has advised numerous financial firms and worked as a partner at Duquesne Family Office, the firm of Stanley Druckenmiller. Warsh is married to the granddaughter of Estee Lauder, who is a billionaire.

In terms of what Warsh said at his nomination meeting, he stated that President Trump had not asked him to commit to rate cuts. Warsh also assured investors that he will not remove current regional FED presidents and simply wants to reform policy, not the institution. He stated that maintaining the FED’s independence is something he deeply believes in.

He also stated that the economic outlook in the U.S. is improving despite inflationary and job market headwinds. Warsh also stated that the economy is nearing full employment. Warsh also went on to blame the FED for its recent politicization, which he wants to avoid. He stated that the expansion of its balance sheet has blurred the line between Central Bankers and politicians. He has long pushed for a smaller balance sheet and believes the FED should not hold long-term treasuries. Critics argue that those purchases blur the line between monetary and fiscal policy by helping keep government borrowing costs lower. If Warsh is confirmed, do not expect rapid change as shrinking the Fed’s balance sheet will be a deliberate and well-orchestrated process. “It took 18 years to create this balance sheet problem, and we won’t be able to fix it in 18 minutes. And so that’s why I think deliberation here is important,” he added.

Overall, the hearing was not surprising, but it did push back the odds that Warsh would be confirmed quickly. One Republican stated that he would not confirm Warsh or any FED nominee until the DOJ drops its investigation into current FED Chair Jerome Powell over his testimony on the Central Bank’s headquarters renovation.

The committee set a deadline of April 23 for written follow-up questions. No vote date was announced.

HPE’s continued momentum

A broadly held holding for our clients has continued its post-earnings momentum over the last few weeks. Hewlett-Packard Enterprise, a multinational technology company based in Texas, reported its first-quarter earnings in the first week of March. In its earnings report, the company reported earnings growth YoY, which also beat street estimates. Revenue came in line with expectations and jumped 18% YoY. The company highlighted its networking segment and improved its fiscal 2026 outlook on its earnings call. A large portion of HPE’s strongest revenue growth stems from its acquisition of Juniper Networks, which closed last year; many expect this unit’s revenue to eventually be most of the company’s top line. Guidance calls for 32–40% non-GAAP operating profit growth, with margin expansion expected as Juniper synergies materialize.

Investors, including us, have been focused on HPE’s positioning in the AI industry, specifically in AI infrastructure. For our longtime clients and readers, this next part is redundant, but for those who are new here: We have liked HPE for quite some time as a rare value play on AI. The company is a profitable AI infrastructure and networking compounder. HPE is a play on the booming demand for infrastructure integrators as inference becomes a bigger part of the AI buildout. The firm is transitioning from a legacy enterprise hardware provider into an infrastructure platform tied to AI and the cloud. HPE is a classic “growth at a reasonable price” company where we are seeing improving margins, increasing free cash flows, and improving profitability at a reasonable multiple. HPE currently trades at 11x forward earnings, and its EV/EBITDA ratio is 7.5x.

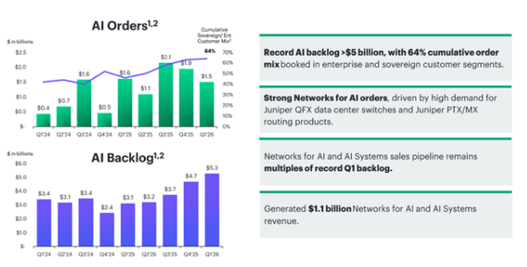

HPE reported a record AI order backlog in its March earnings report, and analysts have forecasted that to increase as demand remains robust and supply constraints impact production for them and the industry. Here is a slide from HPE’s quarterly presentation, which tracks the company’s AI order backlog:

HPE shares have continued their ascent over the last month despite market volatility stemming from the conflict in the Middle East. Shares are up 19% YTD.

We still like HPE shares even with the run they have recently gone on. We think the company remains a strong value play in a high-growth, high-multiple industry. HPE ranks at a four out of five on our risk rating system, which is based on fundamental and technical attributes.

Disclaimer: MacNicol & Associates Asset Management holds shares of HPE across various client accounts.

Vertiv, Vertiv, Vertiv

Vertiv Holdings, a long-time holding of ours, reported its first earnings since joining the S&P 500. Shares slid on Wednesday despite a double beat. EPS beat expectations by 17%, and revenue beat 1%. Vertiv also increased its fiscal year guidance for EPS up to a range of $6.30 to $6.40 from a midpoint of $6.12. Vertiv reported revenue growth of 30.1% with organic growth of 23%, driven by product revenue up 29.5% year-over-year and services revenue up 33.0% year-over-year. Revenue guidance came in line with street estimates. Citi Research analyst Andrew Kaplowitz expects near-term price volatility and stated that shares pulled back despite the beat due to elevated expectations.

For those who are new readers, Vertiv is a play on AI. The company makes critical digital infrastructure for data centers. Vertiv helps power and cool the hardware behind cloud computing, AI workloads, and telecom networks. The company can be seen as a “picks and shovels” play for the AI revolution; demand for their services rises as more servers, AI systems, and data centers are built.

Vertiv has hitched its success to Nvidia, and the partnership between the two companies has become a real catalyst for its market positioning and investment thesis.

We are very pleased with Vertiv’s earnings report and will comment further next week.

Disclaimer: MacNicol & Associates Asset Management holds shares of Vertiv Holdings across various client accounts.

What we are looking at next week

Markets enter the week of April 27th after having paused this week following one of the strongest 3-week stock market rallies on record, driven in part by optimism around Iran de-escalation. That said, the geopolitical backdrop remains the dominant factor, with any escalation posing immediate risk through energy markets and inflation expectations. The upcoming FOMC Meeting next week will be an obvious focal point for investors, despite expectations for no change in rates. Tone and guidance will be the main drivers during Jerome Powell’s question period, with the focus likely to be around geopolitical tensions, elevated energy prices, and the effect that may have on policy decisions.

Investors will go into next week with the current backdrop of uncertainty weighing on Q1 earnings releases, which start to ramp up. Key themes during earnings calls will also be what investors will be watching, as investors will look to see how CEOs are factoring in the unrest in the Middle East, elevated energy prices, the recent issues with private equity, and even the trajectory of AI spend, which appears to be coming down. Taken together, the focus will likely be on whether incoming data and earnings can justify current valuations or if the market’s sharp rally is simply more momentum-driven bullishness after trading sideways for almost 6 months.

MacNicol & Associates Asset Management

April 24, 2026

Download in PDF format: