Share This Post Today!

Voslapp Rear Range Light, Lower Saxony, Germany

This lighthouse is the 22nd tallest lighthouse in the world at a height of 201 feet. The current structure was built in 1907 and remains open. The lighthouse is closed to the public.

Capo Santa Maria di Leuca, Apulia, Italy

This lighthouse was built in 1864 and was lit for the first time in September 1866. The lighthouse stands at 48 meters tall and is operated by the Lighthouses Service of Marina Militare.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Succession plot line

Over the past week, the biggest story in finance centered on Warner Bros. after the company announced a deal with streaming giant Netflix. The agreed-upon deal would give Netflix control of Warner Bros.’ films, television studios, and streaming service (HBO Max). This caught many off guard, including President Trump and industry competitors. The announcement led Paramount, a few days later, to launch a hostile bid for Warner Bros. Paramount’s counteroffer is the latest plot twist in a takeover saga that is likely to upend the Hollywood pecking order. The entertainment arms race continues to heat up and is devolving into the television series Succession (an award-winning show that was based on corporate finance).

Paramount’s CEO is the son of Larry Ellison (Oracle’s CEO). The Ellisons have been leading Paramount since a merger with Skydance Media closed in August. Paramount offered an all-cash $30/share offer for Warner, which equates to an enterprise value of $108.4 billion. Paramount was believed to be the frontrunner to buy Warner before the Netflix announcement (last month, the Wall Street Journal reported that Paramount, Netflix, and Comcast were making bids for Warner). Netflix’s offer values Warner at $27.75/share ($23.25 in cash and the remainder in Netflix stock). The deal implies an enterprise value of $82.7 billion. Netflix has already lined up $59 billion of financing from U.S. banks, led by $29.5 billion from Wells Fargo. Netflix will assume $11 billion in debt from Warner. According to an independent corporate bond research firm, Gimme Credit, Netflix is stretching itself with this planned acquisition. Under current terms of the deal, Netflix’s debt will rise to more than 4x EBITDA (from 1.1x now). Investment-grade company debt ratings typically try to keep this ratio below 3.0x. Netflix debt now has single-A credit ratings—roughly the middle of the investment-grade spectrum—from Moody’s and S&P Global.

Paramount’s deal is reportedly being backstopped by the Ellison family, RedBird Capital, and the debt has been fully committed by Bank of America, Citi, and Apollo. Paramount’s offer also includes investment from the sovereign wealth funds of Saudi Arabia, Abu Dhabi, and Qatar, as well as Jared Kushner’s Affinity Partners fund.

We will say Paramount and Netflix’s offers are hard to compare, as Netflix is not buying Warner’s substantial cable assets while Paramount is. Any comparison of the deal would require determining the value of Warner’s cable assets and a breakdown of debt between the businesses. Paramount’s CEO said they offered a better deal for Warner shareholders, and the company has a responsibility as a fiduciary to consider the all-cash offer. Here are the assets that Netflix and Paramount are targeting:

President Trump took a shot at the Netflix-Warner deal over this past weekend, pointing to Netflix’s potential market share being a major problem on his social media accounts. Trump has also criticized the Paramount deal but has grown very close with Larry Ellison and his son recently.

On Monday morning, Paramount shares jumped higher by more than 7% while Netflix shares slid by more than 4%.

Investors have already worried that Netflix was overpaying in their deal, given that Warner’s streaming revenue has flatlined over the last year. Paramount’s unsolicited offer raises the possibility that Netflix will have to make its offer even more lucrative to Warner. Even if shareholders green-light an eventual Netflix-Warner deal, many worry that the Trump administration would reject the deal. The deal is also expected to receive regulatory scrutiny from European regulators.

Warner Bros said it would review the Paramount offer over the next 10 business days but it was not currently changing its recommendation to its shareholders. As of now, the company is recommending the Netflix deal to its shareholders.

We do not have a horse in this race but are enjoying the drama and increasing deal-making.

Nvidia, Trump, and China

On Tuesday, it was reported that Nvidia had been granted permission to sell its H200 chips to Chinese companies. Trump said in a post that he has notified President Xi that the U.S. will allow Nvidia to ship its more advanced chips to select Chinese customers under conditions that allow for continued strong National Security. According to Trump, Xi responded positively. Trump said his administration is ironing out the final details on the subject, and the government will also allow AMD and Intel to do similar deals.

China banned Nvidia products in September as a negotiation tactic with the U.S. regarding trade. It remains to be seen if China will allow Nvidia to sell its products in its markets. On Tuesday, the Financial Times reported that Beijing has begun discussions on the topic.

According to Nvidia, its current sales forecast assumes zero revenue from China. William Blair analyst Sebastian Naji stated that the sale of H200 chips in China by Nvidia will likely drive upside to the current 2027 revenue expectation in a research note.

The chip that will be available to select Chinese companies from Nvidia is more advanced than the H200 but less powerful than the company’s current Blackwell AI chips. Perhaps allowing a less powerful chip to be sold in China is the correct move for the U.S. If Nvidia sales remain outright banned, Chinese companies will see increased sales, which will provide resources for more research and development, which could eventually lead to some Chinese competitors becoming competitive with Nvidia.

TSX company makes a splash

On Monday, Transcontinental Inc., a Montreal-based packaging, commercial printing, and specialty media company, made a huge announcement. The company announced an agreement to sell its packaging business. The transaction will result in the company’s divestiture in the packaging industry. ProAmpac, a global innovator in flexible packaging and material science, will acquire Transcontinental’s packaging unit for $2.22 billion (CAD). The corporation expects to pay its shareholders $20 per share on Class A and B shares (as of December 5, 2025) if the deal passes. The Transaction is subject to shareholder approval, regulatory approvals, and other customary conditions. Management expects to host a vote by the end of January.

Transcontinental leadership supports the deal and believes the purchase price represents a premium to the value of the packaging business unit and delivers strong value to shareholders. The Chair of the Board went on to say that the buyer is a strong cultural fit for employees, and the business combination will position the company well to deliver increased value to customers.

According to the terms of the deal, the acquisition represents an acquisition multiple of 8.7x the packaging sector’s adjusted operating earnings before depreciation and amortization (EV/EBITDA) as of July 2025. The aggregate purchase price payable to the Corporation in cash is approximately $2.10 billion and is subject to customary adjustments for debt and debt-like items, cash, and net working capital.

The sale of the packaging business represents a significant portion of Transcontinental’s business and will change the company overnight. We have liked shares in recent quarters due to their attractive discounted value. The deal delivers immediate value to shareholders, but the remaining business will more than likely slow growth and a stable EBITDA profile. There will also be some shareholder churn and index implications with this transaction. We are watching very closely.

We will report more information on this topic in the coming weeks, but for now want to keep our thoughts at a very high level.

Transcontinental reported earnings this past week after this publication was written so we will comment on earnings next week.

Disclaimer: MacNicol & Associates Asset Management Inc. holds shares of Transcontinental Inc. (TSX: TCL.A) in select client accounts.

History repeats

As we head closer to the end of 2025, the Federal Reserve made its last policy decision of the year on Wednesday. Before the meeting, there was an 89% probability that the FED would once again cut interest rates according to the CME FED Watch Tool. One month ago, there was a 66% probability of a FED rate cut. If the FED cut, it would be the third straight cut to interest rates. However, some economists believe the decision could be contentious as numerous members of the FOMC who vote on interest rate decisions have questioned a rate cut in recent weeks. Insiders believe three voting members could dissent, which would be the most dissenting votes for an FOMC decision in six years.

On Wednesday, it was announced that the Federal Reserve would cut rates by 25 basis points. This is the third straight cut from the FED despite some objections from key FED officials. The FED cited a weakening labor market as a reason for the cut. As expected, three members dissented. Recent Trump appointee Governor Stephen Miran favoured a 50-basis point cut, as he did at the last meeting, and the Chicago and Kansas City FED Presidents preferred no cut. In the FED’s new median quarterly projections, the FED once again forecast only one cut in 2026 (the same as in September).

In Powell’s speech (which could be one of his last as FED President), he pointed to the data blackout as a major challenge that has prevented the FED from disseminating data. Powell pointed to the FED having very little data on inflation, but once again downplayed tariff-induced price effects so far but said they will begin to show up next year. He mentioned the challenging situation for the FED in the short term as inflation risks are tilted to the upside and employment to the downside.

U.S. markets moved higher after the FED’s decision and during Powell’s speech. It appeared investors liked the move and Powell’s tone at this press conference.

The FED has been arguably making its decisions relatively blindly due to the government shutdown. The government shutdown earlier this fall lasted for 43 days and caused an economic data blackout. There has been a lack of official data on employment and inflation. The FED will have up to three months of backlogged data when it meets at its next meeting in January, which could severely alter decision-making. For example, if inflation has heated up or the job market has improved in recent months, the FED could put further cuts on pause in 2026.

Wednesday’s decision precedes a turbulent 2026 that will see major changes at the Federal Reserve. Chairman Powell’s term as Chairman ends next year (in May) and is expected to be replaced by a Trump loyalist. Powell has been under President Trump’s microscope this year and has caught heat for not cutting rates as fast as Trump wants. The leading candidate to lead the FED is Trump’s leading economic adviser, Kevin Hassett, who supports lowering rates from current levels. The FED Chairman requires Senate confirmation, and many expect Trump’s nominee to face a close vote. Trump’s recent nominee to the FED’s Board, Stephen Miran, was narrowly confirmed earlier this year by one vote.

The changes in the FED have led us and many economists to presume there could be more rate cuts next year as new management at the FED is coming.

There are also growing concerns that the FED has a power structure that is growing. This will test the institution’s independence, especially as Trump and his administration continue to push for further rate cuts.

On the Canadian monetary policy front, the Bank of Canada held rates in place at its last meeting on Monday, highlighting a small jump in inflation and economic resilience as reasons for the decision. Governor Tiff Macklem and the Bank of Canada’s hold of rates was expected from the street. The Bank of Canada stated that third-quarter growth was surprisingly strong but noted that domestic demand was flat. Macklem later elaborated, noting that while certain key Canadian sectors are grappling with steep tariffs, the rest of the economy “continues to operate largely tariff-free” with the U.S. The Bank of Canada indicated in October that its rate-cutting cycle was most likely over when it held rates in place; it held true to that thought on Wednesday.

The Bank of Canada’s next scheduled announcement for the overnight rate target is January 28, 2026.

Critical event for the market and AI

A critical event for markets and AI stocks occurred this week, and it had nothing to do with Nvidia. On Wednesday, Oracle reported its second-quarter fiscal year earnings. These earnings were labeled as critical by numerous analysts for the AI industry and markets as a whole. Oracle shares have been on a roller coaster this year; shares more than doubled from April to September and have subsequently pulled back 38% from 52-week and all-time highs. The database and cloud computing provider has become one of the most important companies in AI and the AI trade.

Investors have recently begun to focus on more than just Nvidia’s chip demand when gauging the status of AI. Wall Street is now concerned about how sustainable the growth in data center demand is. Oracle has been heavily investing in data centers; a slowdown in its investment in data centers could be a stark sign for the AI trade and U.S. indices.

The company is expected to report sales growth of 15% according to FactSet, driven by rapid growth for the company’s cloud and AI software products that customers have adopted as they make their businesses more efficient and cost-effective. Growth is important as investors want confirmation that demand for software remains robust. If the earnings go well, it bodes well for several companies, including Microsoft, due to recent deals that have been announced by companies in the AI industry. Analysts are also focused on guidance and are looking for aggressive guidance that affirms growth expectations.

We are also focused on what Oracle says regarding OpenAI. Earlier this year, the two companies agreed to a 5-year contract, which begins in 2027 in which Oracle will provide $300 billion in software to OpenAI. Investors have begun to question OpenAI’s ability to deliver on its commitments as the company remains unprofitable, and its commitments to purchase services and chips sit in the trillions. If OpenAI cannot make its commitments, it will hit the likes of Oracle hard and potentially burst the AI growth bubble.

The above was written before Oracle reported its earnings. We will review the company’s earnings over the next few paragraphs.

After hours on Wednesday, Oracle reported its earnings. The company missed revenue estimates by 1% and beat adjusted EPS estimates by 64%. Both figures jumped year-over-year (revenue – 14%). Shares sank after hours by more than 10% after the revenue missed expectations and the company released soft guidance for their next earnings report. Investors have been questioning customer demand moving forward and whether revenue commitments will eventually lead to sales. Oracle reported numerous new orders in the quarter, highlighted by deals with Meta and Nvidia. Oracle’s multi-year order backlog grew to $523 billion according to their financials (up $68 billion from last quarter).

Cloud has been driving Oracle’s capital expenditures to new levels—$35 billion over the past 12 months—resulting in free cash losses of $13 billion. The company has used leverage to finance these endeavors, which has many investors worried. Oracle credit default swaps are trading near 16-year highs as investors shift their focus to profitability and converting revenue.

Next week, we will dive deeper into Oracle’s earnings. The two paragraphs above are high-level thoughts after our initial glance at the numbers.

Next week:

Moving forward we will be previewing our following week edition of this publication:

What We Are Looking At Next Week

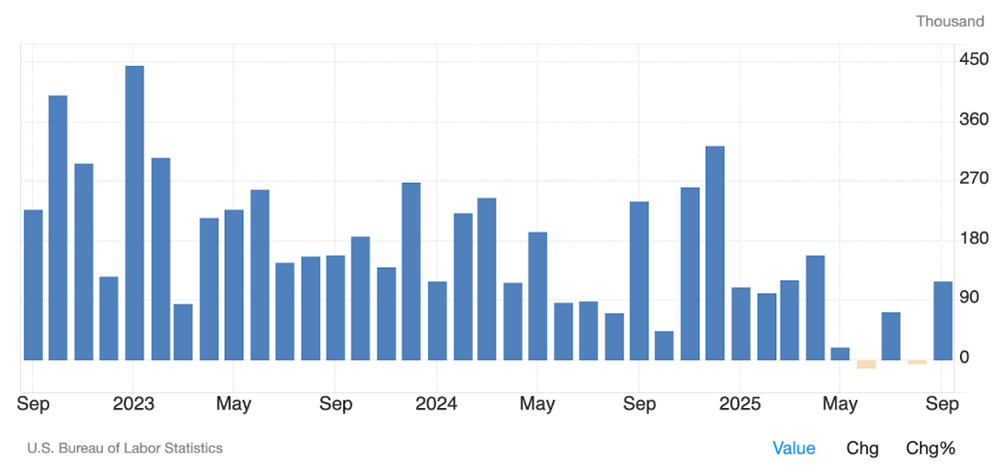

After the longest US Government shutdown in history, investors will get both the October and November US Non-farm payrolls numbers next week on December 16th. With the “data-dependent” Fed having already made their last interest rate decision for the year this past Wednesday, any surprise number could put the Fed in a bind. Non-farm payroll numbers have generally been trending lower, with recent downward revisions producing 2 negative readings in 3 months (Figure 1), something we have not seen since the start of the pandemic.

Figure 1: Poor NFP Numbers next week would align with a jobs picture that looks to be weakening.

A strong reading for both October and November could allay investor fears and even trigger a year-end/Santa Claus rally. If numbers come in weaker than expected, however, we do not doubt that the narrative will shift back to fears about a softer jobs market, a lack of action by the Fed, and ultimately, a recession.

We will be watching these numbers closely to see how they come in and more importantly, how markets react to them.

MacNicol & Associates Asset Management

December 12th, 2025

Download in PDF format: