Share This Post Today!

Vorontsov Lighthouse, Odesa, Ukraine

This lighthouse is a 89 foot tall lighthouse in the Black Sea port of Odesa. It is named after a former governor general of the Odesa Region. The lighthouse originally opened in 1888 but has since been rebuilt.

Tarkhankut Lighthouse, Crimea

This lighthouse is located 5 kilometers southwest of the resort village of Olenivka. The lighthouse was built in 1817 and stands at 108 feet tall. An electrical system was installed into the light station in 1959.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Defiant victory in Japan

Over the weekend, Japan held a national election in which the ruling Liberal Democrats were given the strongest parliamentary majority since World War II. Prime Minister Sanae Takaichi’s coalition received 75% of the Lower House seats. Investors had worried that the snap election would go poorly for the incumbents. However, the election went well, and it appears that there will be a broad fiscal stimulus from the new government, allowing Takaichi to move faster on the domestic agenda.

Takaichi faces the challenge of reviving Japan’s stale economy and tackling the cost-of-living crises.

Takaichi’s agenda has already and continues to put pressure on the Yen. The Yen currently sits near its weakest levels on record against the U.S. dollar. The policies have also led to higher yields in Japan, which are trading at their highest since the late 1990s. Stocks, however, are loving it. The Nikkei 225 is on fire and is near all-time highs.

Many experts believe the positives of Takaichi receiving this mandate outweigh the negatives in terms of impact on markets. The chief investment strategist at Saxo Bank stated, “A supermajority expands policy room on tax relief, fiscal stimulus, defense and industrial policy, but it also increases the chance of policy coherence, flexibility and fewer surprises.”

Debt market experts expect yields to continue to push higher as Takaichi pushes debt-fueled spending. Japan’s debt pile will only grow with this election result. Takaichi’s policies will also more than likely be slightly inflationary, which higher yields could combat. Takaichi’s promises include tax cuts and increased spending on the military. Japan has been battling deflation for decades. This fiscal stimulus could be the juice that fuels the resurgence of one of the world’s largest economies. Takaichi also ran on a platform that seeks to protect Japanese culture and history, which will result in stricter immigration policies despite a declining population.

Another ripple to watch after this election result is Japan’s focus on defense and boosting defense spending.

There is growing support for Japan to defend the Pacific region, especially as China’s “One China Principle” continues to loom. The “One China Principle” is a Chinese diplomatic acknowledgment of China’s position that there is only one Chinese government and Taiwan is a part of greater China. Takaichi has been hard lined against China since coming into politics and wants to directly defend the people of Taiwan. Takaichi has ruffled Beijing’s feathers since winning her first election last year. Japan has been relatively passive for decades when it comes to defense and conflict, but that looks to be changing in front of our eyes.

We think this election result will be bullish for Japanese markets. We continue to evaluate international equities as U.S. markets trade near all-time highs. We also think this election result as a whole is bullish for global markets due to pro-growth policies. It is also bullish for U.S. markets as the Yen continues to break down.

Cathie’s ARK

Cathie Wood is a household name in finance. She has made a serious name for herself over the last few decades. Her notoriety has surged in recent years as her company, Ark Investments, an ETF provider, has grown. Ark’s growth has been fueled by Wood’s popularity and online presence. She is a brash, high-growth investor who makes bold and extremely lofty predictions. For our new readers, this is new information; our long-term readers are familiar with our thoughts on Wood and Ark.

Some of Wood’s bold predictions include her $1 million price target for Bitcoin by 2030, a $2,600 price target for Tesla by 2029, and 40% annual returns for her fund(s).

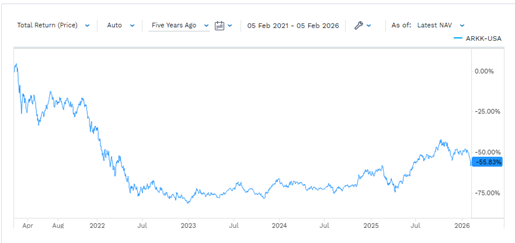

We bring this all up because we recently saw Ark’s flagship ETF performance over the last few years. We knew it was bad, but the real numbers surprised even us. ARKK, which has almost $7 billion in assets, is down over 50% over the last 5 years. As of last Friday, the ETF was down 10 days in a row, it’s longest streak in history.

While ARKK’s value has been slashed in half, the Nasdaq-100 has nearly doubled. Hopefully, you were not caught holding the bag on this overvalued growth investment vehicle. If you want revolutionary technology exposure across a variety of sectors, we would bet on an index like the Nasdaq-100 compared to an Ark fund, despite our negative view on passive investing in today’s markets. Ark’s funds are simply too risky in our opinion.

Alphabet’s debt issuance

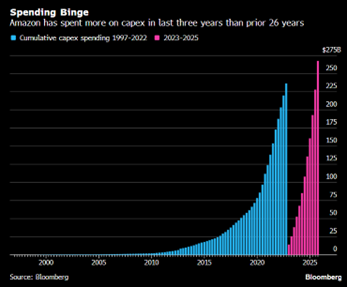

As technology companies continue to roll out their AI initiatives, spending continues to accelerate. An analyst that we follow released data that reflects Amazon’s cap-ex spending. The company has spent more on capex over the last three years than it did over the previous 26 years combined:

This level of spending has begun to worry investors. The worry stems from the simple question of what will fund this spending, and whether it is sustainable.

Oracle credit default swaps have surged in price, Meta set a record alongside Blue Owl with the largest private credit issuance ever, and companies continue to burn cash. The overall trend is something we are following very closely as it is a major risk factor in today’s market.

This week, Alphabet announced a $15 billion bond deal in the U.S. market (the deal was upsized due to robust demand). The issuance comes a week after Alphabet released earnings and stated they will spend between $175 and $185 billion in capex this year (last year, Alphabet reported $91 billion in capex spending). The debt issuance will be priced in dollars, Sterling, and Swiss Francs. Alphabet’s debt issuance in Francs and Sterling is the company’s first-ever offerings in those currencies.

The unusual part of this deal that caught our eye was regarding maturity; according to Bloomberg, the deal will include some notes that will have 100-year maturities. That’s right, 100-year notes. As an investor, how do you possibly forecast 100 years out? Will Alphabet be as powerful in 100 years? A bet like this would go beyond AI and will potentially drive long term meaningful change across the world. However, it also comes with major risks. This is the first time a technology company has tried such an offering since the late 1990s. Alphabet’s 100-year notes will reportedly be issued in the UK and will be denominated in Sterling.

The original deal was reportedly upsized to $20 billion after strong demand and will pay fixed rates with maturity terms ranging from 3 to 40 years in U.S. Dollars, 3 years to 100 years in Sterling, and 3 to 25 years for the Swiss Franc notes. According to news outlets, demand for this issuance reached $100 billion, and the strongest demand from investors was for the 100-year notes. This strong demand reflects the state of capital markets. Demand was so strong that the premium (to U.S. Treasuries) on the 40-year U.S. Dollar notes narrowed to 0.95 percentage points from 1.2 percentage points. The proceeds of these deals will primarily be directed toward building data centers and purchasing high-end servers and AI chips.

Alphabet’s long-term debt exploded from $10.88 billion as of Dec 31, 2024, to $46.5 billion as of Dec 31, 2025. Despite this debt issuance and elevated capex spending, Alphabet Free-Cash-Flow hit a record high last year.

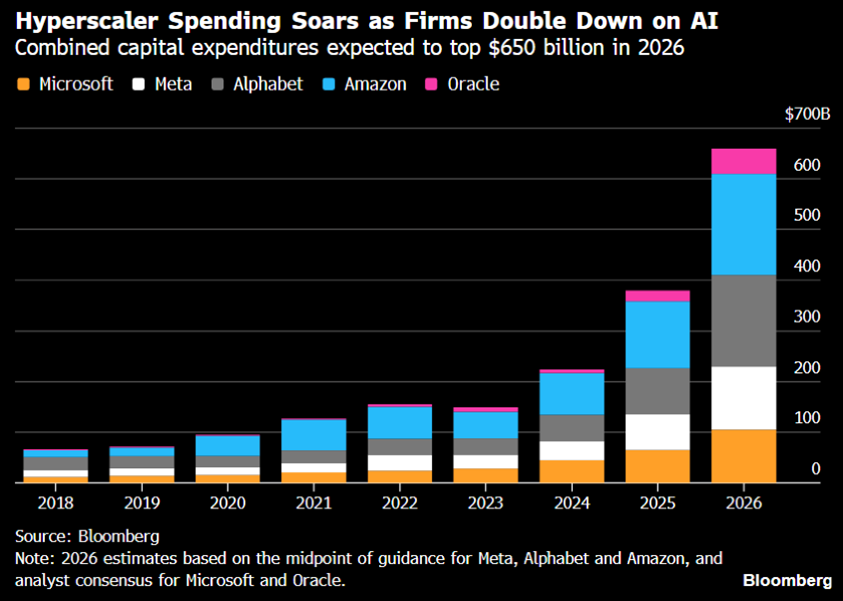

The deal comes a week after Oracle announced a $25 billion deal. Morgan Stanley expects hyperscalers to borrow $400 billion this year, up from $165 billion last year. Hyperscalers are expected to spend $650 billion on capex this year:

Its not just mega cap tech firms tapping debt markets today, Morgan Stanley expects there to be $2.25 trillion in high-grade corporate bond issuance this year.

This level of capex spending from hyperscalers will continue to accelerate until something breaks. Technology inherently innovates, and we expect efficiency to improve down the line when it comes to AI. Is it technologically efficient for AI to consume vast amounts of energy? Not really.

We also believe that some of these technology firms are leveraging themselves up, and it’s a risk factor that is flying under the radar. Just look at Oracle for an example. Tech firms have helped support their stock prices through share repurchases over the last 15-20 years; those programs are slowly shrinking or even disappearing. These firms produced strong cash flows year after year, but for some, those numbers are shrinking. These firms simply need their free cash flow to help finance their capex spending. If the trend continues and something breaks, look out below.

More nuclear tailwinds

The nuclear energy industry has been on a nice run over the last few years. Increased adoption, government support, technology companies securing nuclear partnerships, and the reclassification of nuclear energy as a renewable source of energy have been a few of the reasons driving uranium prices and nuclear stocks higher.

This week, all those drivers helped boost the valuation of a nuclear energy company seeking to go public. According to SEC filings by Holtec International, the company is potentially looking to IPO at a valuation of over $10 billion. This is important because it would be the industry’s largest IPO in years. It also confirms there is widespread demand from investors for nuclear energy.

Holtec International is a Florida-based nuclear company. The company produces equipment used to store nuclear waste and decommissions existing nuclear plants. The company is also reportedly on the verge of reopening an old reactor in Michigan. Holtec has a plan to build and operate its own nuclear power plants; the Michigan plant is its first. The Michigan-based nuclear plant was shut down in 2022, and Holtec was expected to decommission it and store the nuclear waste. That changed quickly after the Michigan government asked Holtec to restart the plant. The plant is expected to reopen in the coming months. Holtec has received county and state assistance in reopening this nuclear plant. Holtec is profitable and reportedly earns over $500 million in an annual income.

Holtec also has deigned a small nuclear reactor and is attempting to get two reactors approved at the Michigan plant. The company was selected by President Trump for a grant to build those small nuclear reactors.

Last year, Barron’s reported that the company was looking to go public in 2026 and would sell approximately 20% of its shares to the public.

The details on this potential IPO are vague right now, so we cannot comment on the company or the valuation. However, we will be paying very close attention when things begin to heat up.

We remain long-term nuclear energy and bullish on uranium prices.

Disclaimer: MacNicol & Associates Asset Management holds uranium mining stocks, ETFs, trust units, and nuclear-themed assets across various client accounts.

U.S. jobs market

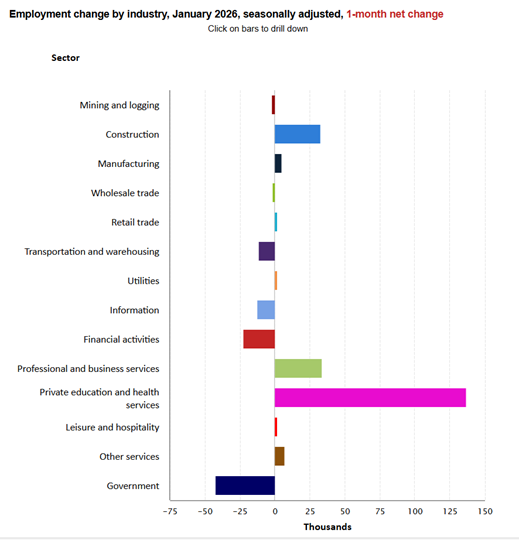

On Wednesday, the Bureau of Labor Statistics released the January jobs report. The report came in stronger than expected as the economy added 130,000 jobs, higher than December’s revised gain of 48,000. January’s payroll gain was more than double what economists had forecasted. David Rosenberg called this the best headline beat in thirteen months. The unemployment rate also ticked lower month over month to 4.3%. The jobs market seems to be stabilizing, which could be a signal for the FED to remain patient on future rate cuts.

The bulk of the job growth was driven by the healthcare sector, which gained 82,000 jobs in January. Healthcare and social assistance have been the only steady industries for job growth for more than a year. Without their gains, the economy would have lost jobs last year. December did show some softening in those areas’ hiring, but that trend dissolved last month.

This jobs report will complicate Trump’s push for lower interest rates as the jobs market is gaining strength. The FED is next due to make an interest rate decision in mid-March. There will be one more job report released before their March rate-setting meeting.

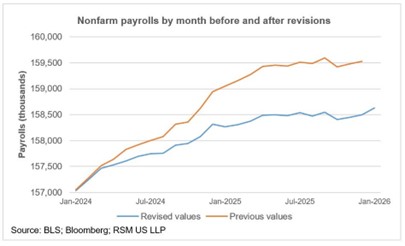

We also received the revised numbers for December on Wednesday. According to the BLS, 2025 was the worst year for job growth outside of a recession (2008, 2009, 2020) since 2003. The U.S. added only 181,000 jobs last year, most of which were driven by the healthcare industry. Without the healthcare industry, the U.S. economy would have lost jobs last year.

Despite the headline strength of this jobs report, cracks remain in the U.S. economy. The jobs market is being dragged along by one industry, and there is major weakness everywhere else. It is also important to note that downward revisions on these reports are common and have happened numerous times over the last year. A downward revision could erase a bulk of January’s gains, which would significantly impact how investors and economists look at these headline numbers.

With revisions, total job gains since the April tariffs are around 12,000, which is statistically indistinguishable from zero.

We will say that January’s jobs report, which was positive on a headline basis, is not being driven by public sector employment and the creation of government jobs; it is private payrolls. The number of federal government employees is now at the lowest level in over 50 years as Trump continues to push for a smaller government:

However, the government subsidizes the healthcare sector in various ways, which artificially inflates employment in the industry. It’s always important to look below just the headline numbers.

Equity markets moved lower on this jobs report, which will likely slow additional rate cuts and reflects some cracks under the hood across the U.S. economy. The jobs market could possibly continue to show weakness or further deteriorate as artificial intelligence improves and replaces employees.

What we are looking at next week (Week of February 16, 2026)

Next week will be a shortened trading week as US markets will be closed on Monday, February 16th, for President’s Day/Washington’s Birthday and in Canada for Family Day. With most major earnings releases for Q4 already out of the way and not much in terms of major economic data releases, investors are likely to focus less on the fundamentals and more on the ongoing changing technical posture of the market. As we have pointed out before, a rotation out of growth has been taking place since October and has recently accelerated (Figure 1).

Figure 1: The chart above shows the relative values of Growth stocks (QQQ) vs. Consumer Staples/Defensives (XLP). The recent swing higher indicates a rotation out of growth and into defense. We saw similar rotations at the start of 2022 and 2025, which preceded large market declines. So far, the market has held up.

We have noted that such rotations typically coincide with declines in the broader market, as was the case in 2022 and the start of 2025 (highlighted). While we have not seen such a decline just yet, what we have seen is the market essentially ‘stall out’, with the growth index, the NASDAQ 100, trading at the same level it has been at since October of last year (when the rotation began), and the S&P 500 trading only slightly higher than those levels. Not surprisingly, the Dow Jones, a less growth-oriented index, has made new all-time highs. Investors should watch to see if this ongoing rotation is simply the market churning through relative valuations, or whether, like in 2022 and 2025, it is a signal of broader weakness to come.

MacNicol & Associates Asset Management

February 13th, 2026

Download in PDF format: