Share This Post Today!

Adziogol Lighthouse, Kherson Oblast, Ukraine

This lighthouse is one of two vertical lattice structures that serves as an active lighthouse in Dnieper Estuary, Ukraine. The lighthouse was originally constructed in 1911 and stands at 211 feet tall.

Cape Hatteras Lighthouse, Dare County, U.S.

This lighthouse was built in 1870 out of brick and reinforced concrete. The lighthouse was automated in 1950 and is one of the tallest lighthouses in the U.S.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Markets wobble

Over the last week, markets around the world began to price in a big piece of news that dropped late last Thursday. President Trump announced he would be nominating Kevin Warsh to lead the Federal Reserve after Jerome Powell’s term comes to an end this spring. Warsh was one of the favourites to be nominated over the last year but gained a lot of momentum last week.

Warsh was a member of the FED from 2006 until 2011 and has been an advisor to Trump in the past. Warsh is a hawkish economist who believes that the FED’s balance sheet should be much smaller. However, experts believe the shrinking of the FED’s balance sheet will be a difficult and slow process. Warsh, who was a Fed Governor between 2006 and 2011, has argued that large Fed holdings distort finances in the economy, and what the Fed now holds should be slashed. Warsh has argued that a bloated FED balance sheet helps the most wealthy and largest firms while it disadvantages small and medium businesses and the rest of Americans.

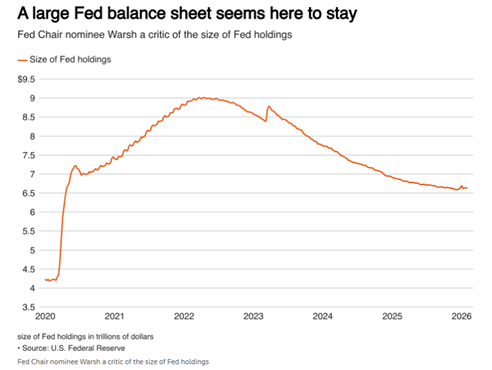

Warsh’s calls to shrink the FED’s balance sheet come at the end of a three-year period where the FED has shrunk its balance sheet. Over the course of 3 years, the FED’s balance sheet grew from $4 trillion to $9 trillion in order to stimulate economic growth.

After Trump made his nomination public, markets pulled back. Losses were led by precious metals, which pulled back heavily. Precious metal prices and companies that mine them have been ripping for over a year. They have been amongst the best-performing assets to start 2026; however, they had a major correction last Friday. Gold prices dropped by more than 9%, and silver prices pulled back by 28%.

Why did this happen, and why did precious metal prices lead the way? First off, we think they were due for a healthy pullback after ripping to fresh all-time highs for what felt like months. However, Friday’s losses were also caused by Kevin Warsh’s nomination, who is an “inflation hawk”. An inflation “hawk” refers to a central banker who prioritises fighting inflation, compared to a “dove” who prioritises growth and jobs. Silver and gold are natural hedges against inflation. With Harsh leading the FED, inflation could become less of a problem down the line. This would impact the demand for precious metals from investors.

It is hard to ignore Warsh and his potential impact on precious metals and equities. However, we believe the movement that we saw last Friday was way overdone and a massive overreaction. This move should not spook investors in the sector, as inflation today remains a problem, and precious metals provide a hedge against numerous other risk factors that Warsh’s nomination will not impact. We think that despite all the noise in the space, miners remain highly attractive today, and spot prices will not move a substantial amount lower. We think spot prices will remain elevated due to continued demand from Central Banks and investors seeking to hedge uncertainty and a weakening U.S. Dollar.

It’s important to note that prices have bounced back slowly in the space since the original pullback. Gold prices have returned to above $5,000, and prices peaked last week above $5,500/oz.

Musk begins to consolidate his empire

Over the past week, Elon Musk announced that he would be consolidating his empire by merging two of the companies that he founded and leads, xAI and SpaceX. The consolidated company creates the world’s most valuable private company, and the deal comes months before the reported IPO of SpaceX.

The deal is reportedly all about AI. SpaceX is reportedly looking to raise capital for its AI ambitions, including building data center capacity. The company recently filed applications with the FCC to build a “space cloud” of up to 1 million satellites. That is 100x the scale of SpaceX’s existing space-based broadband (Starlink). The idea to build data centers in space is to utilize the power of the sun and the cold vacuum of space to free AI from its terrestrial bonds (ie. Electricity supply and cooling).

SpaceX reportedly seeks an IPO valuation of $1.5 trillion, a value that values the company at 60x forward revenue. Elon Musk did not mention valuation in any statements after this acquisition was announced. However, insiders stated that the acquisition values SpaceX at $1 trillion and xAI at $250 billion. Investors in xAI will receive 0.1433 shares of SpaceX for every share of xAI. Some executives of xAI may also reportedly opt for a cash payout over SpaceX shares. Bank valuation documents viewed by CNBC value SpaceX at between $859 billion and $1.26 trillion.

xAI is Elon Musk’s AI startup, which is likely not profitable. This merger will encourage the Musk bulls who would like to see all his companies consolidated. Last week, Tesla disclosed a $2 billion investment in xAI. xAI operates the AI chat box, Grok, and the social media platform X (formerly Twitter). This deal provides xAI with capital as the startup continues to burn cash in order to build out infrastructure against rival labs like OpenAI and Anthropic.

Late on Tuesday, Bloomberg released an article that explored this move and the threat that xAI poses to other AI companies like OpenAI and Anthropic. A large shareholder of xAI and SpaceX stated that this transaction would supercharge xAI’s funding and give it access to more capital than a traditional raise would have. The combined firm would also check numerous boxes and would be able to tap investor bases beyond AI for future capital. The combined entity that could go public could also dampen the demand for an OpenAI IPO.

Top startups, including OpenAI and Anthropic, have struck close partnerships with larger tech firms to stay at the forefront of the global AI race. Musk’s bet appears to be that he can do the same for xAI within his own business empire.

This deal would break a record for the world’s largest M&A deal, once held by Vodafone, which bought Mannesmann in a 2000 hostile takeover.

This is Musk’s latest attempt at consolidating his empire. Last year, he folded X into xAI to give his AI startup access to platform data and distribution. In 2016, Tesla bought SolarCity.

Many experts expect the deal to receive heavy regulatory scrutiny due to conflicts of interest, proprietary technology, movement of engineers, and contracts between entities. SpaceX also holds federal contracts with NASA, the Department of Defense, and intelligence agencies, which all have authority to oversee M&A transactions.

Utility takeover prospect

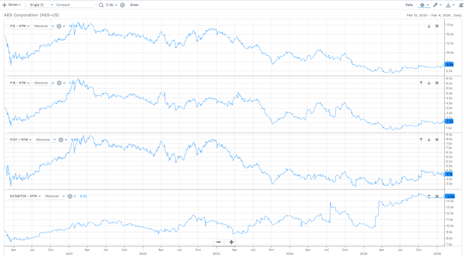

A strong value name in the U.S. utility sector that we like (and own in select client accounts) reportedly has some growing interest from large investors. The company, AES Corporation, is a name we have followed for quite some time. The company is highly attractive from a valuation standpoint and operates in a defensive industry. We have been rotating some capital into defensive names in recent months due to various risk factors present in today’s markets. Despite our rotation into some defensive names, we still look for growth in defensive industries.

AES is a power generation company that is headquartered in Virginia. The company operates in 15 countries with a power generation portfolio that exceeds 32 gigawatts (enough to power 24 to 30 million homes). The firm’s energy mix is diversified with 50% renewable energy, 32% gas, 16% coal, and 2% oil. It sells its electricity to end users and intermediaries like utilities and industrial facilities. AES customers include Microsoft. AES is positioned well in the industry to capitalize on growing demand. According to BNEF, the company is the number one seller of renewable power through PPAs to corporate customers in the U.S. The firm also has market-leading LNG infrastructure, which provides consistent earnings and cash flows.

The stock has had a great last year and still trades at a price-to-earnings ratio below 10x. The firm is highly attractive relative to its integrated utility peer group in terms of P/E ratio. AES trades at 7x forward earnings while its peer group trades at 17.22x (according to FactSet). AES remains highly attractive relative to its historical valuations. The company’s FWD P/E, P/CF, and P/B are near 5-year lows despite the run that shares have been on.

Source: FactSet

Beyond the valuation, and AES being a defensive name with some growth, we like the company from an investment point of view for several reasons. AES has a regulated, diverse revenue base that provides earnings stability and modest EPS growth. The firm has contracted growth in its renewables business segment with corporations and hyperscalers, and structural demand across their markets from data centers and corporations has been able to sustain pricing and backlog replenishment.

On Tuesday, shares jumped after it was reported that BlackRock-owned Global Infrastructure Partners and EQT AB (a Swedish Investment firm) were trying to join up and acquire AES Corp. The two firms could reportedly finalize an agreement for an offer in the coming weeks. BlackRock reportedly had interest in AES back in October. AES announced plans to explore strategic options, including a potential sale, last July after receiving interest from infrastructure investors, but has not found the right price with the right suitors.

Numerous sell-side firms raised their price targets for AES Corp. after the BlackRock-EQT rumors started swirling. It seems a deal is becoming more and more likely. Jefferies noted that the joint bid with EQT changes the narrative in terms of a deal. Last year, BlackRock’s GIP acquired select AES assets, making the street believe that they were not interested in a complete acquisition, but that has seemed to change. Jeffries went on to note that clean energy companies have been trading higher in terms of valuations, which justifies a potentially higher buyout price for AES.

According to Bloomberg data, AES has a market cap of about $11.26 billion and has a firm value of $43 billion, including debt as of Tuesday.

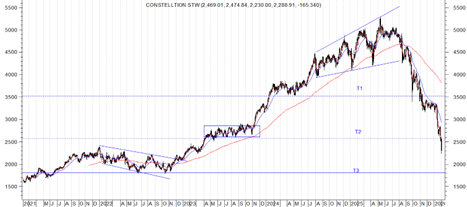

Power providers have been hot takeover candidates with growing electricity demand. Over the last year, Blackstone acquired TXNM Energy, and Constellation Energy agreed to a deal to buy Calpine Energy.

AES Corporation is scheduled to release its fourth-quarter earnings on February 26th, 2026.

Disclaimer: MacNicol & Associates Asset Management holds shares of AES Corporation across select client accounts.

The risk of software

Blink, and you missed a huge trend change caused by AI and its future. AI has been described as revolutionary, groundbreaking, and world-changing technology. The technology will upend workflows, increase efficiency, and potentially lead to issues in society. However, many investors ignored something else that it will impact, software. Software stocks have been some of the best-performing assets of the last few decades; many names have changed the world. However, today they have been left for dead due to AI.

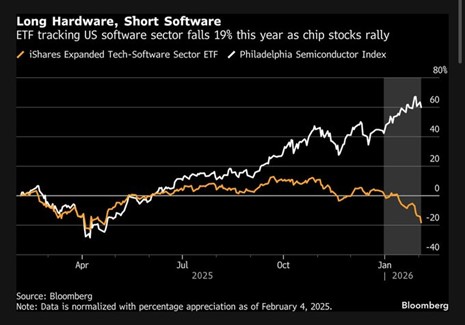

Take a look at the chart below that tracks the iShares Software Sector ETF and the Philadelphia Semiconductor Index (a proxy for AI) since last year. The two groups have decoupled as AI creates new monetization opportunities and has raised concerns about existing software business models.

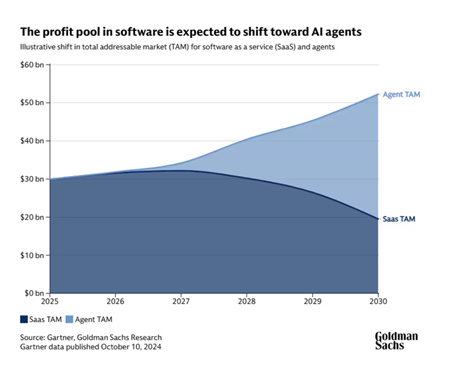

Investors have begun to reprice their valuations of software companies as AI will slow growth, potentially kill software as a service (SaaS), and pressure software companies’ margins. McKinsey surveys show that more than 60% of software vendors expect AI to fundamentally change their business line over the next few years. Goldman Sachs expects profits in software to increase, but expects AI agents to take over the profit pool (Traditional software companies are represented by the SaaS trendline):

We will say not all software companies are created equally, and AI will impact some more than others. Some software companies may benefit from adopting and implementing AI.

If you do not believe us regarding this software trend, check out Constellation Software shares:

Shares are down more than 50% over the last 6 months. We think the company is one of the best in the world at rolling up software companies, and even though it has been hit on the chin. We do believe that this move is overdone and Constellation shares could rebound. However, it underscores the point of risk in software stocks, especially as high-growth investors leave software for the newest and hottest thing, AI.

Jensen Huang hit back at software fears being overblown, stating that AI will utilize existing software rather than creating new tools when completing tasks. If you believe this line of thinking, you can get some pretty steep discounts on big-name software stocks in the public market.

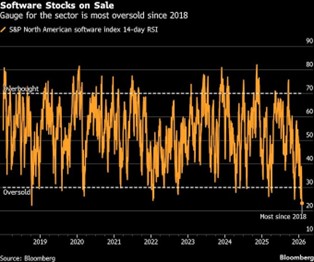

Software stocks are at their most oversold levels since 2018:

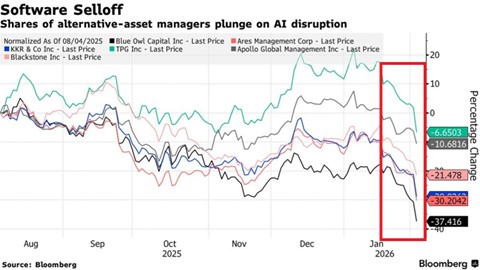

PE stocks collapse

Private equity managers that are publicly listed have seen their share prices melt down in recent quarters.

Why has this happened when public equity markets have roared? This is being driven by a mix of factors, including tariff escalation, sticky inflation reinforcing higher interest rates, fundraising slowdowns, private credit worries, and an exit backlog.

Higher rates are negative for leveraged buyouts and highly levered companies. There have also been private credit issues, which many of the private equity sponsors above are also exposed to. On top of that, there has been a slowdown in exits due to an IPO drought and slower M&A activity. This has led to fewer commitments from investors, which in turn decreases management fees.

We do not own any of the stocks for these alternative asset managers listed above. Our only exposure to the alternatives market remains through our Alternative Asset Trust, which invests directly in private markets. Our Alternative Asset Trust was up 7.4% in 2025, with our private equity exposure running flat over the same period.

What we are looking at next week

For the week of February 9th, 2026, investors will likely be focused on incoming U.S. inflation data, with January CPI setting the tone for markets. At this stage of the cycle, CPI is less about the headline print and more about confirmation: Is inflation convincingly cooling or proving sticky enough to keep policy restrictive? A downside surprise would reinforce the view that the peak in rates is behind us, while any upside pressure—particularly in the core services area—risks pushing yields higher and tightening financial conditions again.

Alongside inflation, earnings remain the second major driver, but the focus has shifted away from results and towards guidance. This week sees a number of major stocks decline materially, not necessarily due to poor earnings but due to management providing poor outlook. Markets are listening closely to how large, index-heavy companies are discussing margins, pricing power, and demand conditions in our ‘higher-for-longer’ rate environment. Corporate commentary that signals resilience justifies the market’s current elevated levels; however, cautious or defensive guidance would challenge the idea that growth can sustain itself as policy remains restrictive.

The two main forces next week—CPI and earnings—ultimately feed into the market’s interpretation of the Federal Reserve’s function. Inflation data tells the Fed what it must do, while earnings and financial conditions signal what it can afford to do next. Layered on top of this is geopolitics, with Iran and broader Middle East tensions acting as a background risk factor. While not a scheduled catalyst, any escalation could quickly show up through energy prices, inflation expectations, and risk sentiment, amplifying moves already driven by macro earnings signals.

MacNicol & Associates Asset Management

February 6th, 2026

Download in PDF format: