Share This Post Today!

Baishamen Lighthouse, Haikou Hainan, China

This lighthouse is located on an island off the coast of mainland China. The lighthouse was built in 2000 and stands at 72 meters tall. The lighthouse has a nautical range of 33 kilometers.

Vittoria Light, Trieste, Friuli-Venezie Giulia, Italy

This lighthouse was built in 1927. The lighthouse stands at 222 feet tall and is fueled by electricity. The lighthouse is located near the Italian-Slovenian border and is one of the worlds tallest lighthouses.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

CoreWeave gets a lifeline

On Monday, AI cloud company CoreWeave announced an expansion of its partnership with Nvidia. The announcement led to CoreWeave shares surging by more than 10%. The expanded partnership includes a $2 billion investment from Nvidia. The two companies said in a joint statement that the investment reflects Nvidia’s “continued confidence in CoreWeave’s business, team, and growth strategy as a cloud platform built on Nvidia’s infrastructure.”

The agreement between the two firms will allow CoreWeave to accelerate the buildout of more than five gigawatts of AI factories by 2030. The five gigawatts of AI data centers are expected to cost approximately $250 billion. Nvidia will get 70% of that in revenue according to Nvidia CEO Jensen Huang. The agreement includes a commitment from CoreWeave to continue using multiple generations of Nvidia infrastructure.

CoreWeave is the largest provider of cloud computing capacity for AI. It has a $55.6 billion order backlog through deals with OpenAI and Meta Platforms. CoreWeave has had a close relationship with Nvidia for years. Nvidia is a supplier, customer, and investor of CoreWeave. Currently, CoreWeave only uses Nvidia chips. The company made its public market debut last year, and shares have been notably volatile. Shares more than quadrupled after their IPO but subsequent questions regarding leverage, valuations, and other risk factors have pushed shares down from their peak. Nvidia will nearly double its ownership in CoreWeave when this transaction closes, making it the third-largest shareholder.

The circularity in AI continues to accelerate as Nvidia continues to embed itself across the industry. Many believed that CoreWeave would need this type of investment to continue operations down the road due to its leverage. With Nvidia’s interest in CoreWeave, this perhaps could be seen as a bailout. The company is sitting on a massive amount of debt and is free cash flow negative. In 2026, analysts expect CoreWeave’s free cash flow to be negative $18.8 billion.

CoreWeave’s CFO has already stated that 2026 capex will be more than double the 2025 figure, and the company could spend up to $30 billion on data centers this year. Demand for data centers remains robust for now, but there are major risks associated with the industry. Goldman Sachs has labeled the financing risk of data centers as tail risk. For us, we distinguish this basket of companies by balance sheet quality and business model.

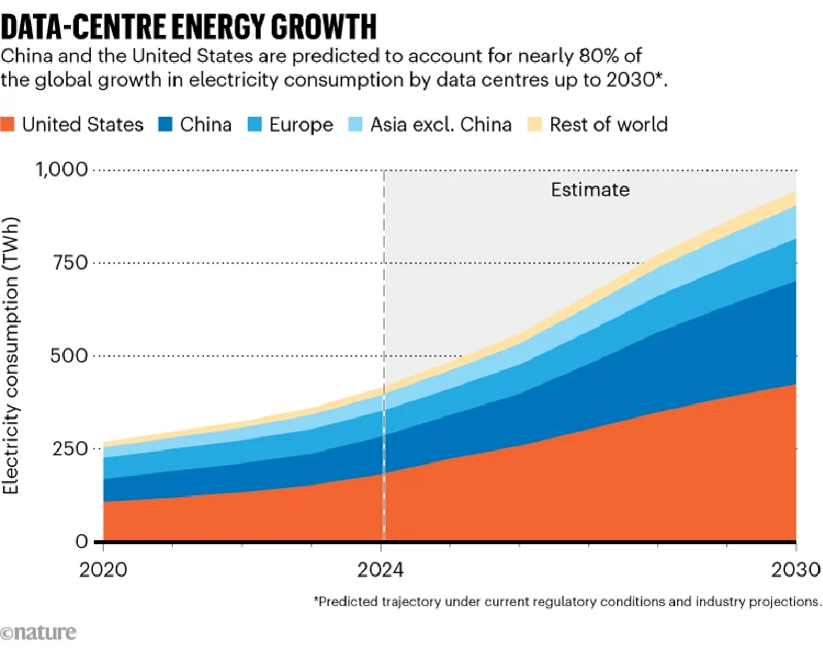

We do not hold shares of CoreWeave as the risk-reward relationship is elevated in our eyes. We continue to believe alternative and corollary industries to AI provide the lowest risk exposure to the growth of artificial intelligence. Data center electricity demand is expected to almost double in the next five years and will reportedly make up 3% of global electricity consumption.

Defense favourite posts strong numbers

A favourite defence stock of ours posted fourth-quarter earnings on Wednesday morning. General Dynamics which we have discussed in the past, is a U.S.-based industrial company that develops and produces advanced military equipment, civilian aviation jets, and provides information technology services.

Our investment case for GD includes several factors. GD is a cash-generating company in a sector that is seeing increased spending due to rising defence and security budgets. Today’s geopolitical climate is complicated, and tensions are on the rise. Countries across the world are sinking tens of billions into defence to secure their borders and protect themselves. President Trump is also a catalyst for increased defence spending worldwide. He has pushed NATO countries to massively increase their defence budgets and has increased the U.S. defence budget. We are also amid a strong business jet cycle supported by record order backlogs. We think GD is well diversified in terms of its four business segments and revenue channels, which limits some of the company’s risk. Finally, we think the company is attractive from a fundamental standpoint. GD trades below median peer EV/EBIT, and EV/EBITDA multiples and trades in line with peers in terms of trailing twelve-month earnings.

On to Q4 earnings.

The company beat street estimates for EPS and revenue. EPS and revenue also increased on a year-over-year basis. GD reported revenue growth in three of its four business segments, led by Marine Systems, which saw a 22% increase YoY. Marine system revenue came in at $4.82 billion versus FactSet’s estimate of $4.18 billion. On a full-year basis, revenue jumped 10.1% YoY to $52.6 billion, and EPS jumped 13.4% to $15.45. Aerospace earnings fell quarter-over-quarter, driven by fewer deliveries, higher overhead and new tariffs.

GD’s order book continues to remain strong as the company had $22.4 billion of orders during the fourth quarter. The company ended 2025 with an order backlog of $118 billion. Total estimated contract value, the sum of all backlog order components, was $179 billion at the end of Q4, a 24% increase YoY.

On the balance sheet, GD cash increased by 37% YoY and long-term debt decreased slightly.

GD released its forward-looking guidance and sees EPS in 2026 in the range of $16-16.20 ($15.45 in 2025) and revenue in the range of $54.3-54.8 billion ($52.6 billion in 2025).

In the question period of GD’s earnings call, management stated they expect margin expansion in aerospace this year, driven by improved efficiency, pricing, and lower overheads. GD continues to see robust demand in defense especially in Europe, driven by geopolitical tensions and modernisation initiatives. The company expects European land systems to outpace other segments through at least 2027.

GD shares initially gapped down on the earnings release but made more than half the loss up through the rest of the day. Shares have been rallying over the last few months, so we think this was a bit of a sell-the-news reaction where some investors took profits. GD also reported some weaker figures in its aerospace segment, which raises some concerns. Forward guidance came in strong, but management raised concerns as margins did not jump substantially. The firm also mentioned some supply pressure.

Overall, we think the decrease in GD’s share price was an overreaction, and the overall earnings continue to paint a bullish picture for GD. Our thesis continues to hold with these quarterly results and the forward guidance.

Disclaimer: MacNicol & Associates Asset Management holds shares of General Dynamics (GD) across various client accounts.

India and the European Union

India and the EU announced a historic trade agreement while North Americans slept on Monday night. The EU and India announced a free trade agreement that is 20 years in the making. The trade agreement aims to double EU goods exported to India by 2032 through reduced tariffs. The deal is historic in size as it creates a free trade zone for more than 2 billion people. The deal signals cooperation in a time of global tension. The European Parliament directly addressed the tension and protectionism seen in global trade when asked about the trade deal. This trade agreement complements India’s deals with Britain and the European Free Trade Association.

The EU is India’s largest trading partner for goods with trade reaching $136 billion last year (12 month ending March 31, 2025). This deal will reduce tariffs for more than 90% of EU goods. The deal will reduce tariffs on automobiles from EU to India from 110% to 10% (up to 250,000 vehicles per year), tariffs on jewelry, textiles, furniture, chemicals, leather, and metals from India to the EU will be eliminated, and tariffs on wines from the EU to India will be cut from 150% to 20-30%. The deal is historic in our eyes.

India is the ninth largest trading partner of the EU, far behind the bloc’s largest trading partners, the U.S., China and the UK.

The deal comes after the European Parliament suspended approval of its trade deal with the U.S. last week following Trump’s Greenland pursuit and subsequent tariffs on some EU nations. This deal is the latest example of countries looking to decrease their reliance on the U.S. by expanding ties with alternative trade partners. The EU has signed deals with the South American trade bloc Mercosur, Switzerland, Indonesia, and Mexico over the last 2 years. India has also been feeling the wrath of the U.S. as Trump imposed 50% tariffs on India last August. India has announced a slew of trade agreements since these tariffs have been imposed, including trade pacts with the UK, New Zealand, and Oman.

This deal will greatly benefit the Indian manufacturing sector. It gives the country greater access to a large market and brightens the country’s economic outlook for 2026. India is a growing nation that is seeing rapid economic growth, thanks in large part to its consumer market. Tariff tensions have remained a large concern for investors when analyzing India due to their export dependence on the U.S.:

Foreign investors have remained net sellers of Indian equities to start 2026. Last year, Indian stocks struggled and had their worst year relative to emerging economy peers in over 30 years according to Capital Economics.

Developed countries are seeking to deepen economic ties with India due to its market being largely untapped. Many expect India to follow China’s economic growth trajectory of the last 20+ years.

In a separate statement on CNBC, India’s natural gas and oil minister stated that the country is in advanced talks with the U.S. regarding a trade agreement and many analysts still believe that a U.S.-India trade deal remains extremely important to India despite this monumental deal with the EU.

This trade announcement comes as India prepares its budget for the year ending March 2027. Investors are hoping the country announces further policies that stimulate economic growth.

We loved to see this announcement due to our view and position in India. We have looked for methods to gain sizeable exposure to India for quite some time and were able to do so over the last few weeks. We think the instrument that we have chosen will benefit from all the strong tailwinds in the Indian economy. Over the last ten years, India has seen rapid change which has been driven by stability, government spending, and foreign investment. Foreign direct investment in India more than doubled from 2014 to 2024. India’s contribution to global GDP jumped from 6% to 8.2% over the same period driven by an 84% increase in GDP. This economic growth was driven by improving regulatory and policy reforms, as well as significant improvements in social health. India has focused on improving healthcare access, water access, nutrition, and sanitation for decades as studies show that when those improve so does economic productivity. India has also tremendously expanded its infrastructure over the last ten years through investments in roads and highways, railways, water purification, data centers, and the overall energy grid.

The security we are talking about is Fairfax India Holdings, an investment holding company listed on the TSX. Fairfax Financial Holdings Limited is the controlling shareholder of Fairfax India. Beyond India’s economic tailwinds, we like this security for a variety of fundamental reasons. The security trades quite cheap relative to other emerging market funds and compared to other Indian securities. Fairfax India’s public portfolio companies trade at a P/E ratio of 16.2x (as of Dec 31, 2024) while the iShares MSCI India ETF trades around 23-24 times earnings. Fairfax India also trades at a much more attractive price-to-book multiple than other Indian assets and its benchmark. Fairfax India shares also trade at a discount to net-asset-value reflecting even more potential upside for the company. The discount has existed for a few years and has narrowed more recently. Many analysts peg the discount to NAV between 12 and 15%. Fairfax India bought back a small percentage of shares in 2025 and are expected to continue to do so in order to decrease the discount to NAV and continue to distribute capital to shareholders.

Fairfax India has diverse exposure to several sectors. Fairfax India is disciplined and seeks to provide long term capital appreciation by investing in public and private securities in India and Indian businesses. Fairfax India launched approximately ten years ago and currently has a market capitalization of $2.5 billion (U.S.). As of the end of 2024, Fairfax India holds $3.6 billion in investments, 70% of which is in private companies. Fairfax India’s largest holding is Bangalore International Airport Limited which is undergoing significant expansion due to rapidly growing demand for aviation services across India. There Indian assets are world class, many of which are monopolistic infrastructure assets.

The company is applying a similar strategy to the one that they have utilized for years in the controlling company. For those who do not know, Fairfax Financial was founded in 1951 as Markel Service of Canada, however, its modern-day routes go back to 1985 when Prem Watsa took control of the firm. The company Chairman, Prem Watsa remains the CEO of the firm and is a Bay Street legend. Watsa has delivered strong returns to shareholders (he remains the company’s largest shareholder, owning nearly 50% of the firm). Fairfax invests in a variety of companies, sectors, and projects across the world. They essentially look for value wherever it can found.

Fairfax’s strong management team have an excellent track record of delivering strong return on equity, we expect that to continue for years to come.

Disclaimer: MacNicol & Associates Asset Management hold shares of Fairfax Financial Holdings and Fairfax India Holdings across various client accounts.

New favourite for FED Chair

Over the last two weeks, a lot has changed in the odds market for who will be the next Federal Reserve Chairman. Current Chairman Jerome Powell’s term comes to an end in May. Trump will be quick to nominate a replacement, one that he hopes will cut rates faster than their predecessor.

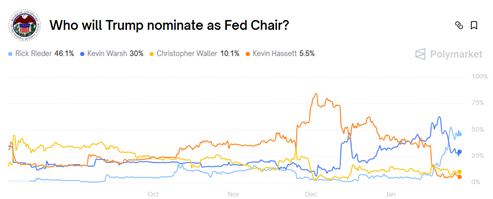

According to Kalshi, there is a 48% probability that Trump’s nominee to be the next FED Chairman will be Rick Reider. Polymarket has similar odds for Reider. However, on December 18th, Reider’s odds sat at just 1.7%, quite the change over one month. For those interested here is the chart from Polymarket that tracks these odds:

For months, we thought the next FED Chairman would be Kevin Hassett or Kevin Warsh, but recently a dark horse has appeared and is all of a sudden, the favourite. Reider is reportedly one of the four finalists to be Trump’s nominee. He has reportedly impressed the administration who reportedly prefer to keep Kevin Hassett in his current role as director of the National Economic Council.

So, who is Rick Reider? Reider is the CIO of Fixed Income at BlackRock. Reider also sits on BlackRock’s top leadership committee alongside CEO Larry Fink. He oversees $2.7 trillion in assets, a number larger than GDP of most countries. He has an impressive track record and resume. Reider is a regular on television and has become a familiar voice to investors and policymakers. His views are widely read by Wall Street according to Barrons.

So why does Trump want him to lead the FED? Reider reportedly shares the same view as Trump that interest rates should be lower. He shares similar views as Trump in regard to affordability and believes the FED is placing too much weight on inflation data that reflect past conditions when conducting monetary policy decisions. Reider has argued that productivity gains from AI, automation and logistics are reshaping the economy in ways that conventional economic indicators capture too slowly.

Reider also believes that mortgage rates remaining elevated reduces turnover, limits labour mobility and slows construction. Trump has made lowering housing prices a priority since returning to office last January. Reider also spoke about how interest rates have an inequal impact in 2024, stating that higher rates weigh most on renters, young families, and borrowers while they benefit high income savers. Democrats have often made this argument regarding rate hikes, and Reider echo’s these thoughts. Perhaps Reider is the goldilocks solution for Trump as a candidate who wants lower rates but does not impact the independence of the Federal Reserve.

Either way you slice it, Reider being confirmed would more than likely increase the number of rates cuts this year.

All this news comes in a week when the current FED and Chairman Powell are due to make their latest monetary policy decision (on Wednesday). Before the meeting, investors, and prediction markets unanimously were forecasting no change to the FED Funds Rate. As predicted, the FED held rates in place as the job market continues to stabilize. Wednesday’s decision follows three consecutive rounds of cuts to interest rates from the FED.

Powell pushed off concerns regarding the labour market suggesting that conditions are stabilizing after a period of steady softening. The unemployment rate improved in December month over month, and the Bureau of Labor Statistics reported that 50,000 jobs were added in the month.

The Bank of Canada also held their benchmark rate in place on Wednesday. This was the consensus belief as the BOC has already cuts rates at a much faster clip than other Central Banks across the world.

MacNicol & Associates Asset Management

January 30th, 2026

What We Are Looking At Next Week

For the week starting February 2, 2026, it has become clear that investors next week will be focused on the violent shift in the precious metals space. Both gold and silver saw their largest single day declines in decades after President Trump announced Kevin Warsh as the next Federal Reserve Chair. The move signals more than just position unwinding—it reflects a sudden reassessment of the monetary regime, particularly around Fed independence, credibility, and the future path of real rates. Markets are now testing whether the multi-year precious metals uptrend has reached an inflection point.

This matters because gold and silver have both been the market’s clearest barometer of political and monetary distrust. The speed and magnitude of the sell-off suggests that investors are at least entertaining the possibility of a more orthodox, credibility-driven Fed under new leadership, even amid elevated geopolitical risk. Whether this move proves durable or merely a violent reset will depend on follow-through: stabilization would imply consolidation within a broader secular trend, while a continued decline would signal a meaningful shift in inflation and policy expectations.

With that said, investors will still be cognizant of earnings season, which remains active in the background. Large-cap and bellwether stocks report next week and their results (and guidance) will influence index-level performance. Given the developments of Friday, however, their impact will likely be filtered through rates and currency dynamics shaped by the emergent Fed narrative. In short, the meat of earnings season will remain important, but we will be watching to see how the developments in precious metals sector set the tone moving forward.

Download in PDF format: