Share This Post Today!

Lighthouse of Praia da Barra, Ilhavo, Portugal

This lighthouse is located off the west coast of Portugal’s northern region. The lighthouse stands at 203 feet tall and was built in 1893. The original plans for the lighthouse were approved in 1879 and the lighthouse was planned to be much shorter.

Cordouan Lighthouse, Gironde, France

This lighthouse is located 7 kilometers at sea off France’s west coast. The lighthouse was originally constructed 1611 and was eventually automated in 2006. The 221-foot lighthouse is one of the tallest in the world.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations. *

Media empire splits

On Monday morning, Warner Bros. Discovery announced that it would be splitting itself up. The media giant is splitting into two publicly listed entertainment companies in a tax-free transaction. One company will include its movie studios and HBO Max, its streaming platform, and the other will include all its cable channels, including CNN and TNT.

Shares jumped over 7% on this news.

The cable-focused entity will hold a 20% stake in the streaming and studios business. The company will use those earnings to pay off its existing debts.

Warner Bros. Discovery’s CEO will be the studio and streaming company’s CEO, while its current CFO will head up the indebted cable-focused entity.

Warner expects the transaction to close in mid-2026 subject to board approval.

The company signaled that it was open to breaking up last year when it announced plans to restructure to shareholders.

Numerous entertainment companies have been pursuing these types of breakups in recent years. Firms want to separate their high-growth streaming businesses from cable CTV which has seen ratings, and revenue slumps.

Comcast announced plans to spin off its cable networks late last year and SkyDance Media is expected to carve out some of its cable channels if it can close its merger with CBS’s owner Paramount Global.

The spin-off could be a little late as economic conditions continue to tighten and many consumers could begin to cancel their streaming subscriptions to save money. The spin-offs also will not solve the cable problem. This rebrand will not change the fact that Warner Bros. Discovery’s cable assets are under pressure. The entire industry has been under pressure as advertising revenue declines and more and more customers cut the cord on cable.

We will not be buying this jump but will continue to watch this transaction along with the industry very closely.

Diversifying out of America

We have mentioned throughout this publication’s history that diversifying your exposure to equities is important. Despite the massive run U.S. equities have been on, it is important to have a global approach to equities. We have long invested in markets across the world including Canada. We think the relative outperformance of U.S. stocks will slow and global equities could go on a nice run (on a relative basis).

We bring this all up this week because of a decision made by the CEO of the world’s largest company. Nvidia’s CEO spoke at London Tech Week on Monday and announced that the company will be making investments in the UK AI ecosystem stating, “it is an incredible place to invest and I’m going to invest here.”

We know not to read too deeply into a speech by a CEO but it’s confirming a trend. Companies are looking global, and investors should do the same. We are not saying sell all your U.S. exposure, we are saying diversify your exposure just like companies are.

Nvidia also announced several artificial intelligence initiatives as the conference kicked off, including establishing a U.K. sovereign AI industry forum together with British companies such as BAE Systems, BT, and Standard Chartered.

Nvidia shares opened higher on Monday after the speech. British equities are trading near 52-week highs so now might not be the time to dive all in on them. However, the British along with many other European equities continue to trade at relative discounts compared to American equities.

Circle success

Last week, we mentioned the IPO of Circle Internet Group, a cryptocurrency firm that issues one of the world’s largest stablecoins. The IPO launched after this edition was completed so we wanted to talk about its trading performance since.

The oversubscribed IPO was a huge success, and shares soared after going public. Shares briefly touched $138/share during pre-trading on Monday after going public on Thursday at $31/share. However, shares pulled back to $110 by lunch on Monday. If you’re buying now, you could see some pain in the short term, however, you could also see some huge returns. Either way, it will be a volatile ride.

Expect a lot slower crypto and other firms operating in the industry to go public while the asset class is hot.

In other Circle news, according to a filing from Circle Internet Group, 50% of the company’s revenue goes to Coinbase. The deal between the two firms will last more than 3 years according to filings.

From what we have read Circle Internet Group arguably operates like an uninsured money market fund that is leveraged.

We will continue to watch the company but at this valuation, we will remain on the sidelines.

In other crypto news, BlackRock’s spot Bitcoin ETF is the fastest ETF to ever surpass $70 billion in AUM. This chart shows the explosive growth and adoption of the new-age asset class. Ironically this is occurring when gold prices also continue to soar. Perhaps there is a place for both assets in investor portfolios.

We ran a chart this week that paints a bearish case for Bitcoin prices. According to Bravos research, the number of new addresses used to store Bitcoins plunged to its lowest level in 5 years. The last two times the number of new Bitcoin addresses fell by this amount, and Bitcoin prices fell by 70% the following year.

During past cycles, this relationship meant more as retail investors predominantly drove demand for Bitcoin and were at one point the only groups buying the asset. This time around, institutions have begun and are continuing to buy Bitcoin which has created a heavier concentration in Bitcoin ownership. Fewer wallets, larger purchases. So perhaps the number of new addresses buying Bitcoin is not a factor that should be followed from now on.

Housing hits the brakes

Housing prices have leveled out in recent months as consumers battle with tightening economic conditions and elevated prices. These trends have led to record homes for sale in numerous markets. Even the hottest markets which have seen massive population increases in recent years are not immune to this trend. According to ResiClub there are five times more residential units for sale in Dallas versus in 2021.

We promise homeowners and investors that there will not be five times more demand than in 2021. Do not expect home prices to replicate their 2017-2022 performance moving forward. We think especially in residential there could be a period of consolidation where incomes catch up to home prices.

One chart

We wanted to share one chart this week published by ChartR. The chart tracks monthly visits to Wikipedia and ChatGPT. ChatGPT officially overtook Wikipedia a few months back and the spread will certainly grow.

This chart tracks the base case for AI for an average consumer. Consumers often used Wikipedia to gather simple facts when conducting research, they are now using a more powerful tool, ChatGPT. This application is one of the simplest forms of AI. Obviously, there are more growth avenues for AI as a whole and this chart shows consumers are willing to adapt and will not drag their feet when it comes to AI.

U.S.-China trade talks

This week the U.S. and China will be conducting trade discussions in London. According to insiders, discussions got off on the right foot. Over the weekend, China’s Commerce Ministry said it had approved some export licenses for rare-earth-related products, a move the U.S. saw as a goodwill gesture.

The discussions come after President Trump and Xi talked over the phone last week. Investors will hope the positive momentum continues between the leaders of the world’s two largest economies. Last month China and the U.S. agreed to pause most tariffs between the two countries.

According to Chinese government data, U.S. shipments dropped 35% in May year over year, the biggest drop since the start of Covid-19. This drop in purchases will significantly impact the Chinese economy which is heavily dependent on exports.

On Wednesday morning, President Trump announced that China and the U.S. had created a framework for a trade deal. The deal was negotiated by high-level government officials from both nations in London and is subject to both Trump and Xi’s approval. As a part of the deal, the U.S. will get access to Chinese rare Earth metals and Chinese students will be allowed to apply and attend U.S. universities. In terms of tariffs, the countries agreed upon 55% tariffs for the U.S. and 10% tariffs for China. Trump stated that the relationship between the two nations is excellent in a statement on social media.

Futures moved higher on this news as real progress looks to have been achieved between the U.S. and one of its major adversaries. We will have to see if the deal gets signed and what is in the deal when details emerge.

In other government news out of the U.S., it seems the bromance between Elon Musk and President Trump is fractured for the time being as the two men took shots at each other via social media. The conflict began when Elon Musk came out against Trump’s “Big, Beautiful Bill” which will expand the deficit. Musk has long been critical of bloated government spending. It is the reason he has spearheaded DOGE. We are in the same nonpartisan camp as Musk on this issue, you simply cannot continue to run these deficits. It’s unsustainable and will just kick today’s issues down the road and pass along major issues to the next generation.

Another wrinkle of this conflict and the proposed Trump-backed Bill will impact Tesla. Trump wants to cut the EV mandate which gives EV buyers a $7,500 tax credit. Trump says Musk only came out against the Bill when he heard that the EV credit would end, however, Musk has pushed back.

The conflict has gotten so bad that Musk claimed Trump would have lost the election without his assistance which the President pushed back against.

For now, it does not seem like the Bill will pass as is. The Bill needs to pass in the Senate and will reportedly require 60 votes which would include numerous Democrats. However, who knows with Trump, he could attempt to pass it through some other method in the Senate.

Either way, a fascinating drama between two of the world’s most powerful men. Tesla shareholders have taken the conflict directly on the chin as shares have slumped by almost 15% over the last five days (as of June 9th).

Bonds, bonds, bonds

We have talked about the risks associated with investing in long-term bonds for over 10 years now. The low-interest rate environment that we have been in limited the return of these securities but increased the risk in our eyes. That is why we have sat on the sidelines in debt markets for the most part in recent years. We know our thesis has been proven right as the bond market has had some very bad years (2022) as Central Banks hiked interest rates to multi-decade highs to combat surging inflation.

We bring this all up this week not to be repetitive but because of a chart, we ran by this week. Over the last 10 years investors in the iShares 20+ Year Treasury Bond ETF have lost money. If you invested $10,000, 10 years ago, and held until today you would have $9,500. This calculation includes dividends and is not adjusted for inflation.

Quite the medium to large sample size for why you probably should limit your long-term debt exposure. We think the risks that we have mentioned that have plagued debt markets over the last 10 years still exist today and investors will have to battle against other risks including lower investor demand for sovereign debt as they move forward.

We think investors should take a multi-faceted approach to credit and incorporate numerous sub-asset classes in their fixed-income portfolios. We would also recommend that investors avoid long-term traditional bonds unless they have a very long-time horizon in regard to their portfolio.

Gold, gold, gold

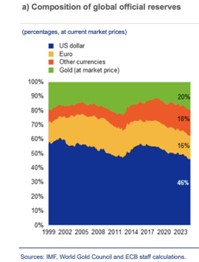

As gold prices have increased, Global Central Banks have benefited greatly as they have significantly increased their exposure to the precious metal over the last few years. According to the International Monetary Fund, gold has overtaken the Euro as the world’s second most important reserve asset:

Gold now accounts for 20% of global official reserves, the highest percentage in a decade. Central Banks have heavily been buying gold since 2022 as they rotate away from the Dollar, and Euro and into physical gold.

Unfortunately for us Canadians, our government sold off most of our golf reserves back in 2016.

When Canada sold most of their gold in 2016, they were an outlier, most large Central Banks were buying the asset. Gold was trading in the $1,200 range in 2016, quite a failed sale by the Canadian government.

We think this added demand from governments creates a floor for the price of gold that is much higher than in previous cycles. We remain bullish on gold moving forward for numerous reasons including the stability, inflation protection, and physical applications of gold. Investor demand is also driving the price, and it seems for now purchases from investors, institutions, and governments will continue to occur under these economic conditions.

MacNicol & Associates Asset Management

June 13, 2025

The Weekly Beacon -June 13 2025