Share This Post Today!

Point Penmarc’h Light, Penmarch, France

This lighthouse is located off the northwest coast of France. The lighthouse is one of the tallest in the world. The current structure was built in 1897 and was eventually automated in 2007. The tower is open to the public. Reaching the top takes climbing 307 steps, 227 stone steps followed by an iron staircase.

El Rincón Lighthouse, Buenos Aires Province, Argentina

This lighthouse is the worlds 19th tallest traditional lighthouse in the world. The concrete lighthouse was originally constructed in 1925. The lighthouse has a nautical range of 29 miles.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Trump makes a call

In early trading on Monday morning, stocks moved higher and energy prices moved lower after it was reported that other countries would join the U.S. effort to secure safe passage through the Strait of Hormuz. Trump refused to name the allied countries that would be assisting the U.S. The Wall Street Journal reported that the U.S. could announce as soon as this week that along with a coalition of countries they have agreed to protect and transport ships through the Strait which is currently being guarded by Iran and preventing most traffic from passing through the waterway. On Tuesday, the Wall Street Journal reported that Japan, Australia, and Germany will not be sending ships to assist the U.S. in the Middle East and France, and the Uk are still weighing their options.

The three main U.S. indices reached their lowest levels since November last Friday as investor fears of a prolonged Iranian conflict grew. Higher energy prices impact companies worldwide, as energy products are major inputs and costs for many industries. Even with Monday’s oil price pullback, the price of oil per barrel remains well above $90 and is nearly $30 per barrel more than it was just a few weeks ago. Energy Secretary Chris Wright said Americans may feel the impact of high gasoline prices “for a few more weeks,” in an interview on NBC News on Sunday.

Oil prices have surged since Israel, and the U.S. began their direct conflict with Iran. Many fear that energy prices could alone lead to higher inflation rates and prevent the FED from slashing interest rates. The FED is due to make its latest monetary policy decision this week. Alongside the Fed, the Bank of Japan, the Bank of England, and the European Central Bank are all set to host their latest policy meetings this week. The FED is not expected to change interest rates at this meeting, but investors will be focused on forecasts from Central Bankers, specifically if the war in Iran has changed their stance. As of December, FED officials projected only one rate cut in 2026. Right now, with current trends and energy prices surging, we would expect that to come to fruition. Higher interest rates for longer, something we have been talking about since 2022, when rates were originally hiked to combat inflationary pressures stemming from the COVID-19 stimulus and the Ukraine-Russia conflict.

On Wednesday, the U.S. Bureau of Labor Statistics released its latest producer price index data, and prices are moving….

The producer price index for final demand rose 0.7% in February from January, compared to economists’ expectations at 0.3%. Expect this number to jump more as the data incorporates higher energy prices stemming from the Iran conflict.

Private credit redemptions

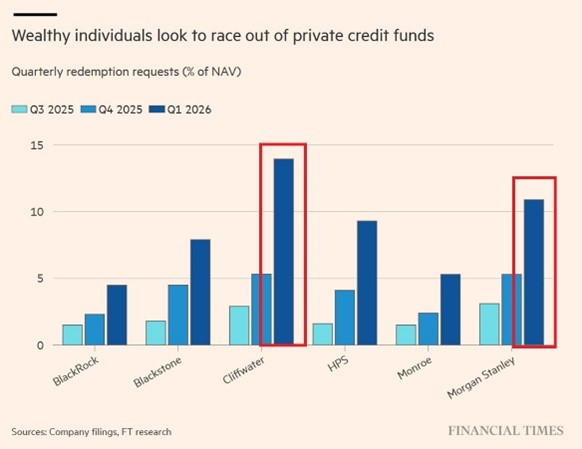

According to the Financial Times, investors are still rushing to redeem their private credit fund holdings. Wealthy individuals have requested over $10 billion in withdrawals from large private credit funds in 2026. These redemptions have tripled since Q3 2025, with every major manager in the industry seeing an increase in redemption requests.

According to the Financial Times, only 70% of the requested redemptions by investors will be granted, as investors will be forced to deal with the illiquidity of the asset class. Investors will be stuck in these funds as managers are forced to put up their gates. We expect many funds to continue marking some loans to loss.

This private credit meltdown has led to the sponsors of major funds seeing their stock prices (in public markets) sharply pull back. Blackstone, KKR, Ares, and Apollo shares are all down more than 25% year-to-date. This pullback has wiped out more than $100 billion in market value across the industry and is being driven by loan losses, lower fees, and major redemption requests.

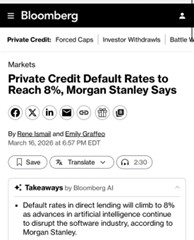

The poor performance of these private market managers has led financials as a sector to have their worst start to a year since 2020, according to Bloomberg and Yahoo Finance. Strategists at Bank of America said investors as a whole are growing concerned with financial stocks, including U.S. banks. According to Morgan Stanley, direct lending default rates are expected to reach 8% due to AI disruption. Credit fundamentals of software loans are challenged with the highest leverage and the lowest coverage ratios across major sectors, and defaults are only set to climb further as AI disruption unfolds.

Many U.S. banks have exposure to similar loans as private credit funds, and defaults have begun to rise. In a Wall Street Journal article, Patrick Corrigan, a law professor at the University of Notre Dame, stated, “Banks are at the center of this system even when they appear not to be.” This trend has led hedge funds to rapidly dump their financial exposure in recent months.

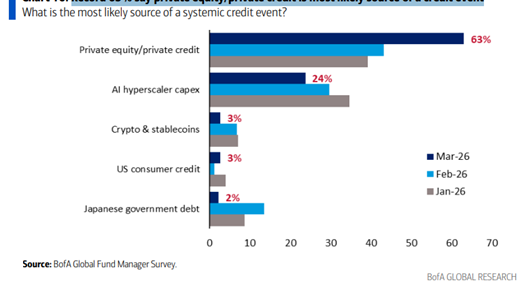

According to Goldman Sachs, hedge funds are now shorting financials at a pace not seen since 2016. The Bank of America Fund Manager Survey states that managers believe that private markets are the most likely source of a large credit event (and those worries have surged over the last month as loan losses and redemption requests have grown).

Some investors have compared this private credit situation to the early days of the Great Financial Crisis. Private credit was once one of the largest growth engines for Wall Street and has now become one of its largest anxiety points. The real reason this might be an issue for investors is that many of these private credit giants are heavily leveraged to software companies that are seeing their MOATs disappear with the emergence of artificial intelligence.

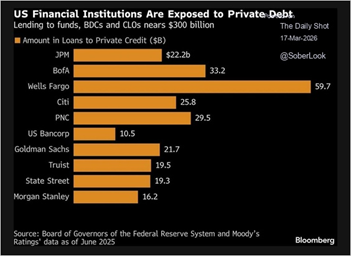

Here is a graphic from a Bloomberg article that outlines the private credit exposure of large U.S. banks:

Although these numbers are negligible when compared to each bank’s assets, they are impactful when combined, especially when paired with private credit exposure at other types of institutions.

We expect these worries to continue as institutional allocators and even wealth managers slow their allocation to private credit and closely monitor the sponsors of private credit funds. However, at one point, the reward will outweigh the risks for the sponsors of these funds in public markets as valuations and fundamentals are becoming increasingly attractive. We will be looking very closely at finding potential opportunities; we will warn that it could take some time, as sponsors will be slow to realize loan losses.

Nvidia’s new target

NVIDIA hosted its annual GTC event this week in San Jose. The event, according to many, is the premier AI conference across the world. At the event, Nvidia made a bunch of announcements highlighted by a new forecast for chip revenue for the three-year period ending in 2027. These announcements were made by Nvidia CEO Jensen Huang, who spoke for over two hours on Monday.

The company now forecasts $1 trillion in sales from Blackwell and Rubin chip sales by late 2027. This number is double what the company’s prior forecast was ($500 billion through 2026). Wall Street applauded this statement and saw Nvidia shares move higher in Monday trading. This revenue forecast also suggests its overall data center revenue, which includes other products, could be well ahead of Wall Street expectations. In the last 12 months, the data center segment has had sales of $192 billion, up 66% from the previous period.

NVIDIA also unveiled a new hardware system aimed at inference, generating output from AI models. NVIDIA said that this new system can generate 700 million tokens—the basic unit of computing measurements—per second, or 350 times as fast as NVIDIA’s previous Hopper generation of graphics-processing units. This new inference system should assist Nvidia in fending off custom chips from the likes of Google’s Tensor Processing Units.

NVIDIA also got many investors excited with AI robotaxi hopes. NVIDIA’s self-driving business unit is valued at $1.2 trillion by Morgan Stanley. The companies’ autonomous driving solutions are reportedly chipping away at Tesla in the industry. NVIDIA’s DRIVE platform aims to bring AI into the real world, turning any car into a robo-taxi, with its DRIVE AGX Thor computer and a suite of predefined sensors, including cameras and laser radar. NVIDIA’s DRIVE platform is already being adopted by Uber, BYD, and more. Uber’s fleet of DRIVE-enabled robo-taxis will launch in 2028.

Elon Musk is reportedly not worried about Nvidia’s DRIVE program, but many believe he should be, as a chunk of Tesla’s valuation is attributable to its future robo-taxi business unit. If Nvidia commoditizes this technology, it could cause Tesla’s valuation to significantly compress.

Commodity boom

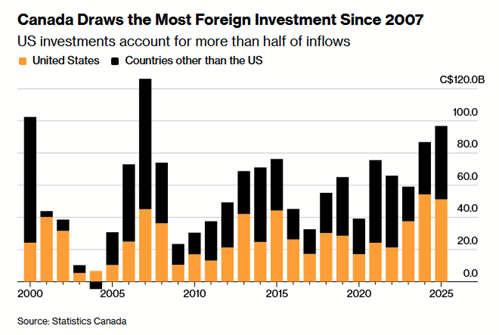

As commodity prices have surged, inflation worries remain, and as uncertainty continues to plague the global economy, investors have searched for hedges and alternatives. One of our favorites has been commodities or commodity-producing companies that trade at attractive valuations. A major benefactor of this trend has been Canadian markets, which have a heavy exposure to natural resources and commodities based on the Canadian economy’s tilt towards commodities.

According to Bloomberg, foreign direct investment in Canada reached an 18-year high last year. A majority of that investment came from the U.S. fourth quarter investments were driven primarily by M&A activity.

In 2025, net investment into Canada exceeded net outflows by $17.4 billion. The surplus is a major reversal from 2022, when $49.3 billion in investment exited Canada.

Despite weakening economic fundamentals and similar policy stances to the former administration, Canada’s new administration has attracted capital due to its cheap valuations across the country and the commodity boom that we are seeing unfold in front of our eyes. We expect this to continue as investors diversify away from the U.S. after a 15-year outperformance period for U.S. markets.

According to TD Economics, as of 2024, the U.S. is Canada’s largest foreign direct investor, and Canada is one of the U.S.’s largest.

Franco’s blowout

After the recent precious metal run, earnings for many precious metal mining and royalty companies have exceeded investor expectations. For our investors, this has been great news as we have been overweight with miners for quite some time now. We have believed for a long time that precious metals would move higher due to a variety of factors (we have talked about this thesis in depth throughout this publication’s history). This belief led us to overweight quality precious metal companies over the years.

One company that reported earnings last week which we wanted to touch on this week is a long-term holding of ours, Franco-Nevada (FNV). The dual-listed company is a royalty and stream play. The company owns a diversified portfolio of cash flow-producing assets. Precious metals make up 85% of the company’s revenue, most of which is gold. FNV’s other commodity interests are in other metals and energy commodities. FNV is the world’s largest royalty play in the gold space. The company’s assets are diversified across the world, but 75% of the company’s revenue is sourced from the U.S., Canada, and South America. Here is a slide from Franco-Nevada’s February corporate presentation, which displays the company’s assets across the world (as of Jan 31, 2026):

Source: Franco Nevada Corporate Presentation February 2026

The company had a record year in 2025, according to management. In terms of the company’s 2025 performance versus guidance, the firm achieved its production levels set forth. The record year and strong cash flows led FNV to hike its dividend by 16% in January. The firm has kept its balance sheet debt-free and remains in a strong position in terms of available capital ($3.1 billion) despite making a handful of acquisitions over the last few months, including four this year. This puts the firm in a unique position to be able to continue deploying capital and creating shareholder value.

For the fourth quarter, the firm beat revenue estimates according to FactSet by 11%. The firms’ adjusted EBITDA and EPS also beat street estimates. The firm’s adjusted EBITDA margin came in at 90.6%, and its adjusted net income margin came in higher than expected at 59.6%.

In terms of guidance, management stated that production will increase this year, driven by the addition of new assets and the ramp-up of other existing assets. The firm stated that higher precious prices continue to drive margin expansion. They also stated that for every $5 increase in the price of WTI (oil), there will be a 7% increase in energy revenues. Non-precious metal revenues account for 10% of FNV’s revenue, the majority of which is crude oil. The firm will continue to pursue low-risk royalty plays in geographic jurisdictions where operational risk is low. Management also stated that the firm will continue to look to diversify revenue through nonprecious metal and energy assets “in order to balance cyclical commodity exposure and enhance resilience”.

FNV’s guidance does not include any contributions from Cobre Panamá. First Quantum is still waiting for approval to stockpile ore, which would result in stream deliveries to FNV of 23,100 gold ounces and 265,000 silver ounces (current guidance for 2026 comes in at a range of 510,000 to 570,000 GEOs). Should production restart at the Cobre mine there is potential for materially higher GEOs, depending on the conditions of such a restart. Based on the average of the next 5 years of the mine plan, which was in place at the time of suspension, the stream has the potential to contribute as many as 150,000 to 175,000 GEOs to Franco-Nevada annually once at full capacity. This further underscores the potential upside, down the line, for FNV shareholders. The current outlook, even without Cobre, is strong; the added production potential of the Cobre asset has been described as a free call option for FNV shareholders by some mining analysts, and we agree with the sentiment.

We continue to like the hedge that FNV provides to our shareholders. We continue to look for new entry points in the position on a technical basis. We will state that FNV is exposed to numerous risks, including commodity, pricing, macro, and a lack of operational control at the actual mines. FNV is a security that belongs in certain (risk appetite-dependent) well-diversified portfolios.

Disclaimer: MacNicol & Associates Asset Management holds share of Franco-Nevada (FNV) across various client accounts.

March 20, 2026

MacNicol & Associates Asset Management

What we are looking at next week:

Investors head into the week of March 23 with growing concern that the market may be rolling over into a broader correction. The S&P 500 is now testing its 200-day moving average, a level widely viewed as a key dividing line between longer-term bullish and bearish trends. Historically, sustained breaks below this level have been associated with deeper drawdowns, which puts added weight on how price behaves here. The technical setup alone is enough to keep investors cautious, particularly after a period where momentum has already weakened.

This fragility was reinforced following the latest decision from the Federal Reserve and comments from Jerome Powell, who held rates steady but emphasized that the economic impact of the ongoing Iran conflict remains “uncertain.” That uncertainty was not well received, with markets pushing the S&P 500 to a new low for the year, underscoring how sensitive current conditions are to ambiguity around growth, inflation, and geopolitical risk — leaving investors focused on whether the market can stabilize at these levels or if further downside confirms a broader correction is underway. Next week, investors will be watching closely for signs that conditions are either beginning to stabilize or continuing to deteriorate beneath the surface.

Download in PDF format: