Share This Post Today!

Chipiona Lighthouse, Andalusia, Spain

This lighthouse is located near the southwest border of Spain. The lighthouse is one of the tallest in Europe and was originally built in the 19th century. The lighthouse can be seen 129 kilometers away and flashes every 10 seconds.

Nosy Alañaña Lighthouse, Madagascar

This lighthouse was built in 1932 out of concrete. The active lighthouse is the tallest in Africa and is located 16 kilometers north-northeast of Toamasina. The island that the lighthouse sits on is only accessible by boat. The site is open to the public.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Oil limit up

On Monday morning, oil prices surged with Brent trading above $80 a barrel, up 8.6% from Friday, and West Texas crude trading 7-8% higher (Crude moved another 7% higher on Tuesday morning). This historic energy price spike was caused by last weekend’s Israeli and American strikes on Iran. Equity markets around the world pulled back after these strikes.

The Israeli’s reportedly killed the Supreme Leader of Iran, which caused Iran to retaliate in its own way. Israel responded by targeting Hezbollah targets in Lebanon (Iran and Hezbollah, the terrorist group, are seen as allies in many world circles). The response by Israel widens and escalates the conflict, which led to energy prices resurging after they had pared some of their gains overnight.

Why does this Middle Eastern conflict impact oil prices so much? For one, this heightens geopolitical risk across the world. This conflict has already spread across the region as Iran hits back. Saudi Aramco shut production down over the weekend at an oilfield in Saudi Arabia due to debris flying in the air from drones being intercepted (according to the Saudi Ministry of Energy).

The Middle East is also one of the world’s heaviest oil-producing regions; a new conflict could impact production and even shipments. Iran being directly involved in a conflict is also big for financial markets and energy markets. The country has minimal allies, completely opposes the West, and is the 6th largest oil producer (2024, worldometer) in the world.

An Iran – U.S. / Israel conflict is tricky to forecast. The conflict could be a series of strikes with no direct military on the ground, or it could be a multi year drawn war with troops on the ground. We are not government nor conflict experts, so we will not speculate; we will only talk about markets.

Before we move any further, we wish the people of Iran well and hope they finally get the change they have long desired and deserve.

Iran reportedly cut off the Strait of Hormuz in response to the U.S. / Israel strikes. The closure of the Strait is massive for oil markets. Approximately 20% of the world’s oil passes through here, which will halt vessel transit and heighten supply concerns around the world. Analysts have warned that oil prices could spike if the closure is prolonged. JP Morgan’s head of global commodities stated that vessel transit on Sunday through the Straight came to a standstill, marking the first near-complete halt in its modern history.

On Monday, OPEC+ released a statement stating it would hike production to combat these price increases. The OPEC+ cartel of oil-producing nations, meanwhile, agreed to hike output by 206,000 barrels a day from April.

Natural gas prices also moved higher this week as Qatar suspended production at a key LNG plant on Tuesday morning. The plant was shut down due to a drone strike. The Dutch TTF front-month contract rose 35.7% on this news. Qatar is the worlds third largest LNG exporter. Many believe that North America and Australia will ship more LNG to offset the Qatari shortfall, but that prices will remain elevated while energy facilities are threatened.

Other than moving global oil prices higher, this conflict and decrease in Iranian production will impact China the most. China has for years relied on the likes of Venezuela, Iran, and Russia for its energy imports. China gets this oil off the books at a discount, according to many industry experts. China buys more than 80% of Iran’s shipped oil in 2025, according to Kpler. Iranian oil has limited buyers due to U.S. sanctions aimed at cutting off funding to Tehran’s nuclear programme. China’s Iran oil imports accounted for 13.4% of the country’s oil imports last year. Reuters calculates that Iranian light crude trades at a $6 to $10 per barrel discount. Similar discounts were available in Venezuela for the Chinese. Those discounts add up when you’re buying millions of barrels per day.

This cheaper and off-book oil makes China more competitive and makes it harder for countries around the world to compete with it. Oil is an input in thousands of industries, lowering the price of oil increases margins or decreases selling prices. This is something Trump has attempted to combat.

In January, the U.S. seized control of Venezuela’s energy assets after arresting its President; this month, they assisted Israel in its attack against Iran. China relies on both those nations for cheap oil; they are Chinese allies. Although the U.S. opposes Iran and Venezuela’s old leadership, their moves seem to have a deeper meaning that correlates with other interests, including the opposition of China.

Do not take this lightly; we are in a new technological cold war, and the U.S. just took a shot and landed it.

Energy, shipping, and defensive stocks moved higher on this news. Markets were led by energy tankers, which trade at flea market-level discounts. Energy tankers transport energy products across the world.

History tells us what?

In the piece above, we mention oil and energy prices spiking and equity markets moving lower after Iran and Israel / the U.S. spar in the Middle East. There has been growing fear that this conflict will boil over and that there could be grave consequences for the world, the global economy, and financial markets. We certainly hope that is not the case and wish people across the world our best.

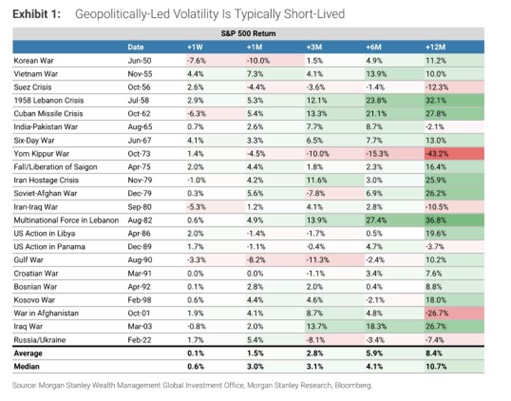

We bring this all up because we ran by a Morgan Stanley Wealth Management Global Investment Office chart that outlines the forward performance of the S&P 500 after geopolitical events. The chart shows that geopolitical-led volatility is typically short-lived. The S&P 500 was up on average 8.4%, 12 months after a geopolitical event. Obviously, there are anomalies on both sides of this data set, and it deserves further investigation; however, it is a great reminder of the resilience of investors and financial markets.

A geopolitical event does not mean it’s a doomsday by any means for financial markets. Morgan Stanley’s above research went on to say that unless oil spikes in a historical manner, this conflict will not change their bullish view on equity markets for the next six to twelve months.

No matter what way you look at it, we think there were some major overreactions in financial markets to start this week.

Slam the breaks on private credit

Investors continue to flood sponsors with redemption requests in private credit funds. There have been major redemptions in the booming private credit space since late 2023. These redemptions have exposed the structural liquidity limits, even though credit performance has not cracked in a systematic way. Investors have also seen a few major loans that have gone belly up in the space. There has also been a slowdown in deal-making, which has slowed capital deployment and exit opportunities in private markets.

Private credit has exponentially grown since the financial crisis, as an industry that, with tighter regulations, caused banks to slow their lending.

We bring this up because of an article that was written this week by Barron’s. Barron’s reported that Blackstone’s private credit fund (BCRED) has seen record redemptions, and experts believe worries are growing across the industry. Blackstone’s private credit fund allowed investors to redeem 7% of its assets in the first quarter, resulting in $1.7 billion in net withdrawals. This percentage exceeded the 5% limit that Blackstone had set. These mass redemptions follow a similar story seen across the industry. Blue Owl Capital sold $1.4 billion in assets and halted redemptions in its private retail debt fund last month.

JP Morgan analysts noted that the indicated redemption requests in the first quarter saw a notable uptick compared to the previous quarter. They also stated that this is an industry-wide trend and is affecting more than just Blackstone and Blue Owl; it has impacted Apollo, Ares, and many more.

Private market-focused firms like Blackstone and Apollo have been affected by the AI induced software sell-off, as the firms are highly exposed to technology and software companies.

Correlation, or causation?

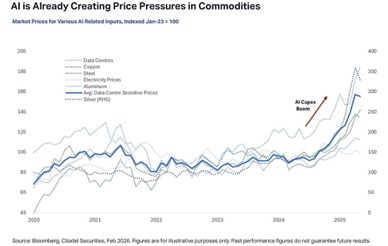

Many market participants, including us, have warned that the growth of AI and the expansion of data centers will lead to higher commodity prices (at least in the short term). From a fundamental point of view, demand for many commodities is growing across the world as companies invest in AI. Supply simply cannot keep up. Eventually, perhaps supply and demand return to an equilibrium, which is not today.

According to Bloomberg and Citadel Securities, the recent commodity surge that we have seen has been caused by the growth of AI:

Demand for copper, silver, steel, aluminum, power generation, and data center infrastructure has surged over the last year. This has led to higher prices for each commodity or input. We do not think that is a coincidence. While many bought Nvidia, Apple, and Oracle in order to capitalize on the AI trade, we have focused on commodities and utility providers. We think these are safer AI plays than buying growth stocks for 50+ times earnings (especially in today’s market environment).

Buying the world

According to Bank of America, only 26% of global equity flows in 2026 are going to U.S. funds. This is the lowest level in 5 years, and a sharp decline compared to the last 4 years. The world went on a buying spree in U.S. markets due to the success of the Magnificent 7 and the FAANG stocks. These stocks now trade at elevated valuations and are spending at will on AI capex. This spending has investors worries and investors are now finally looking for non-U.S. exposure (in size).

We have been saying that there are better opportunities globally, and investors should consider exposure to other developed markets and select emerging markets. That is exposure is a reason that we outperformed U.S. markets over the last 12-18 months.

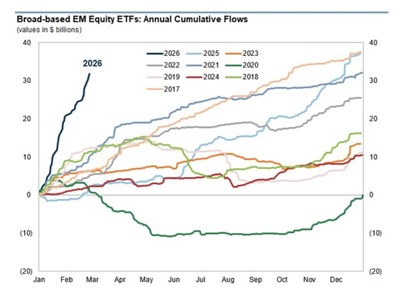

This decrease in U.S. inflows has not impacted overall equity allocation. According to Bank of America Global Investment Strategy, global equity funds recorded $38.1 billion in inflows last week. Global equity funds are expected to have $1.1 trillion in inflows this year, surpassing the 2025 record of $826 billion. Although investors are worried, they are not changing their allocations dramatically. They are making small tactical decisions and diversifying their equity exposure. According to Barchart, emerging market-based ETFs have seen record inflows to start 2026, where investors have bought $32 billion in EM ETFs in the first 2 months of 2026.

We expect that pace to slow down, but the overall trend of investors rotating to international equities to continue.

Disclaimer: MacNicol & Associates Asset Management holds shares of domestic and international equities across client accounts. These instruments include closed end funds, ETFs, and individual stocks of developed and emerging markets.

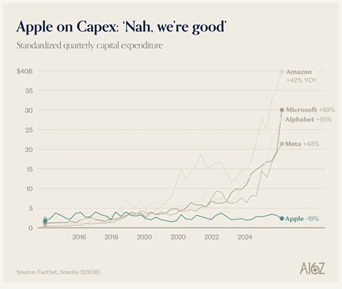

Apple passing on a bubble or punting on AI?

Much can be said about hyperscalers and their investment in capex in today’s markets. Companies are investing hundreds of billions in AI data centers, power generation, and semiconductor chips. The company’s leading the way are amongst the world’s largest companies, including Amazon, Microsoft, and Alphabet. Big tech has found their next major endeavour, and they are all piling in, all but one that is. Apple has not spent heavily on AI capex and does not (as of now) plan to do so. Apple’s capex spending actually shrunk on a quarterly basis by 19%.

The company is spending the least on AI but is still benefiting from this new technology. The company’s hardware and products continue to sell out, and many have labeled their devices as AI infrastructure. Apple is effectively monetizing AI through device demand and a robust operating ecosystem.

The Apple model is less capital-intensive and allows the company’s balance sheet and cash flow to remain strong. Although Apple shares have lagged their big tech peers in recent months, we are certainly monitoring the company and its share price.

What we are looking at next week:

As discussed earlier, Iran is likely to be the main topic for investors next week. The market enters the week with the geopolitical risk still very much elevated after the U.S. and Israeli campaigns in the Middle East, and retaliation efforts on both sides intensified. Unsurprisingly the conflict has affected energy prices, but next week will likely serve as a period to determine if this is simply a near-term spike, or whether this conflict will result in an extended period of higher energy prices.

From a scheduled data perspective, next week will see the release of U.S. CPI on Wednesday, a release that will likely influence rate expectations and fixed income positioning. While unlikely to be factored into this print, the recent increase in energy prices will likely loom large on subsequent inflation releases, meaning that next week’s numbers will likely set the stage for the rest of the year.

March 6, 2026

MacNicol & Associates Asset Management

Download in PDF format: