Share This Post Today!

Adra Lighthouse, Adra, Spain

This lighthouse is located on the southern coast of Spain. The original structure was built in 1899. The structure that stands today was built in 1986 and was the third structure constructed at the light station. The lighthouse stands at 26 meters tall.

Cabo Prior Lighthouse, Galicia, Spain

This lighthouse is located off the western coast of Spain overlooking the Atlantic Ocean. The lighthouse was constructed of stone in 1853 and is operated by the Ferrol Port Authority.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Market roar

After a weak month in which equity markets pulled back to multi-month lows, driven by the conflict in Iran and overall market volatility, markets rebounded heavily on Monday morning. This rebound was driven by optimism stemming from talks between Iran and the U.S. According to President Trump, the two sides discussed the matter over the weekend and are seeking a resolution. Trump also announced that the U.S. would be pausing further strikes on Iranian power plants and energy infrastructure. This would potentially bring stability to the region and, more than likely, decrease energy prices.

Iran’s state-run news agency denied that these conversations occurred, citing the Iranian foreign ministry. The ministry stated that Trump’s comments were early and were a way of lowering energy prices.

Despite very different claims from each side, it seems that the market liked Trump’s comments more. Perhaps investors liked a pause on the energy infrastructure strikes as it would signal a deceleration in tensions, or perhaps Monday’s move was a rebound that we have been due for, as the market has been in heavily oversold territory for quite some time.

Market breadth was particularly strong, with only 45 members of the S&P 500 moving lower as of lunchtime on Monday.

Despite this sense of optimism from the Trump administration, energy prices jumped on Tuesday (reversing Monday’s drop). This comes from news that Slovenia has begun fuel rationing, and the New Zealand government announced weekly tax credits to nearly 150,000 families. We also think that the recent price movement of oil reflects a much higher floor despite Trump’s rhetoric. We think energy prices will more than likely be higher for longer, just like interest rates have been. Macquarie Group’s global energy strategist stated that even if tensions dial back, the price floor for oil would be in the range of $85-90/barrel (much higher than before the conflict began).

The whirlwind that is the Trump presidency alters financial markets daily. It is as important as ever to remain disciplined and remove emotion when making investment decisions. So far in this cycle, institutional investors have been unwinding and derisking their portfolios while retail investors have largely leaned into weakness, according to Mark Hackett, CMO at Nationwide.

Polymarket traders put the implied odds of a cease-fire between Iran and the U.S. before the end of April at 51%, up from 38% before Trump’s announcement.

Private credits cracks

Over the last few months, we have been reporting on the private credit space. Once the hottest asset class in markets and a growth engine for Wall Street has now become a giant thorn in institutions and investors’ sides. Bad loans, paired with deteriorating fundamentals has led to underperformance across the asset class. This, along with other market risks, has led many investors to redeem capital. Investors have major concerns as credit quality weakens across the asset class due to major exposure to vulnerable sectors like software.

These issues for private credit funds have even led to rating agencies cutting the ratings of a few private credit funds. This week, a private credit fund jointly run by KKR and Future Standard saw it’s rating cut to junk by Moody’s. Moddy’s cut was attributed to continued asset quality changes. Expect many of these “low risk” funds and assets to get rerated to “high risk” as loan losses build and investors head for the hills.

The only issue for investors is that these funds mostly lack liquidity and have been forced to suspend redemptions. Even the largest asset managers in the world are facing liquidity crunches and are feeling the impact of loan losses and mass redemption requests. Firms that have suspended or limited redemptions include BlackRock, Blackstone, Morgan Stanley, Blue Owl, and more. On Tuesday, Ares also announced that it would be limiting redemptions on its $10.7 billion private credit fund. Apollo also announced limits on redemptions for its $25 billion Apollo Debt Solutions this week. According to Barron’s, Apollo investors sought to withdraw 11.5% in net assets during this past quarter (the fund limits redemptions at 5% per quarter). According to Bloomberg, these redemption limits and suspensions have yet to trigger a margin call.

Across the industry, investors have submitted $11.7 billion in redemption requests from more than half a dozen major private credit funds, but only 66% of withdrawals have been met.

We bring this all up this week because over this past weekend, Blackstone reported its first monthly loss in over three years in its flagship private credit fund in February. The funds return for February was -0.4%, nothing huge, but a trend break that we think could be the start of something much larger. According to the Financial Times, the fund wrote down the value of a select number of loans during the last month. Among the firms, write downs was customer service software firm Medallia, according to reports.

Blackstone’s flagship private credit fund has $82 billion in assets and allows investors to redeem a portion of their capital every quarter. The fund saw record withdrawals in the first quarter of this year.

This trend has led to the shares of many private market asset managers like Blackstone having large drawdowns in recent months. Blackstone shares have lost more than 28% of their value so far this year. Many of the shares of these private asset managers are selling below their net asset values while many of their private fund’s trade at 100% of NAV. We think many institutional investors are potentially sniffing around, looking for high-quality assets for cheap or a potential arbitrage opportunity.

Loan losses have ticked up across the board in private credit, which has led many U.S. banks to tighten their lending to private credit funds.

JP Morgan marked down the value of certain loans to private credit funds this month. JP Morgan also stated that it will reduce lending to the funds. According to Reuters, JPMorgan’s credit agreements for private credit allow it to re-mark valuations based on the collateral of the fund. This move by JP Morgan essentially limits the leverage of the underlying private credit sponsors. Reportedly, JPMorgan went through its portfolio line by line and put different marks on each loan.

Banks are now even offering exposure to investors who want private credit to blow up. According to a Bloomberg article last week, JP Morgan and Goldman Sachs are now offering hedge funds a way to short private credit as the asset class continues to deteriorate.

We believe loan losses in private credit will continue to rise as credit conditions tighten and many borrowers face refinancing pressures. In our view, a significant number of loans and portfolio company valuations remain overstated, masking underlying credit deterioration. As redemption activity picks up, we expect these dynamics to force more accurate marks, revealing the true health of certain portfolios. This process could lead to renewed volatility and negative performance for underlying investors as valuations adjust closer to fair value.

Monumental occasion

A longtime holding for select clients of ours had a big day on Monday. The company, Vertiv Holdings, has been talked about in this publication in depth. It is an AI beneficiary that provides infrastructure and services for data centers, communication networks, and commercial and industrial environments. The bullish case for Vertiv depends on the growth of AI, data center construction, and the firm’s positioning in the sector.

As AI spending has spiked and hyperscalers have committed hundreds of billions to data centers, AI stocks have boomed, including Vertiv Holdings. Vertiv shares are up 177% over the last year and even more since investors recognized Vertiv’s AI story. Vertiv has also gotten a recent lift despite market weakness due to its inclusion in the S&P 500. An inclusion of a stock in a major index forces passive funds and managers to purchase shares of the company.

Vertiv has been able to capitalize on increased spending in the sector, specifically for liquid cooling and power management systems used in AI data centers. The company also has a big endorsement in the sector, Nvidia. It has been in Nvidia’s partner network since 2024, and the firms continue to work on joint projects to increase the efficiency of their technology. Most recently, the firm reported very strong quarterly earnings and provided solid guidance when it released earnings in early February.

Vertiv joined the index on Monday as part of the S&P 500’s quarterly rebalancing. There were three other additions this quarter, including Coherent, EchoStar, and Lumentum Holdings.

We will say the lift that Vertiv got from index inclusion is probably complete, and shares are trading at the upper end of its 52-week range, so a pullback could be likely in the short term. However, we are a long-term investor with a multi-year view. We have long believed Vertiv is a cheaper and lower risk way of playing AI than many of the chip makers and hyperscalers and continue to support that thought. However, we are watching the sector and the company closely, especially in today’s volatile and high-risk markets.

Disclaimer: MacNicol & Associates Asset Management holds shares of Vertiv Holdings (VRT: NYSE) across various client accounts.

Deleveraging

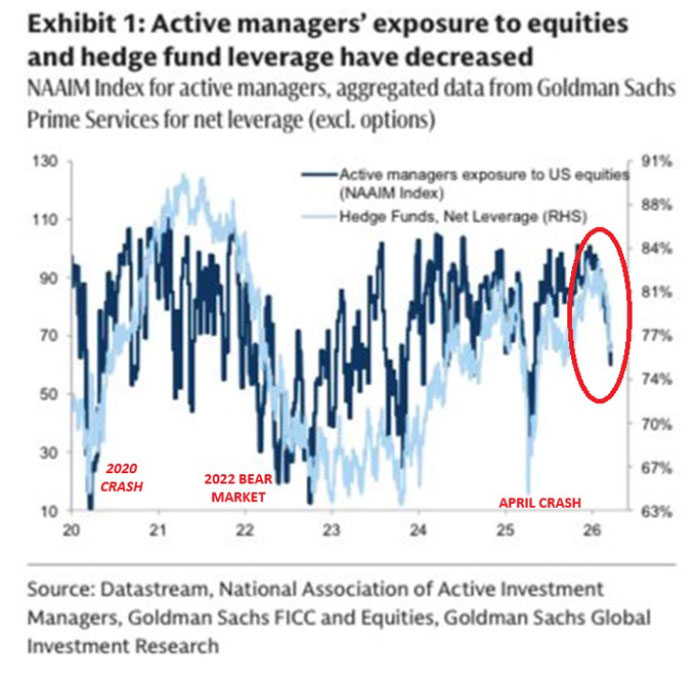

According to a graphic from Datastream, Goldman Sachs, and the National Association of Active Management, active managers’ exposure to U.S. equities, as well as leverage for hedge funds, has decreased over the last 3 months. Both indices are now at their lowest levels since April 2025, when Trump introduced broad-ranging tariffs on ‘Liberation Day’.

Both of these indices are rapidly decreasing and are signs of both investor risk appetite and sentiment regarding U.S. equities. Both seem to be deteriorating, and we think it’s being driven by various factors, including the conflict in Iran and the ballooning private credit problem, which is flashing major warning signs. Investors are derisking away from the most expensive stocks and decreasing their leverage. The rotation away from U.S. equities has been unfolding for months, and we expect this trend to continue. This rotation is a major reason that we have been seeking alternative equity markets over the last 15 years.

Buying opportunity

Gold prices have surged over the last 18-24 months. However, in recent days, the price pulled back. The dramatic pullback has led to an overreaction by many retail investors. The price of gold as of Tuesday morning was set for its worst 5-day stretch since 2013. Gold futures dipped below $4,400 an ounce on Tuesday, its 5th straight down day according to Dow Jones Market Data. Over that 5-day period, gold prices have dropped by more than 12%.

The pullback has been driven by volatility and paper market sales. The strengthening U.S. dollar has also negatively impacted precious metal prices. Precious metals are an alternative store of value to the U.S. dollar. Despite gold’s safe-haven characteristics, investors have looked for safety in the U.S. dollar since the conflict in Iran began. The U.S. dollar has also benefited from energy price increases, as inflation could prevent the FED from slashing rates.

Despite the weakness in financial markets, gold demand reportedly remains robust in the physical market.

We think this price pullback is an opportunity for investors underexposed to gold and other precious metals. This price movement is completely overdone and could possibly reverse in the coming months. We will say that this price movement has more to do with broader market movements, a natural correction, and investors’ deleveraging their portfolios than the thesis of gold changing.

We continue to believe that gold belongs in investment portfolios and will allocate accordingly to the market environment.

Disclaimer: MacNicol & Associates Asset Management holds shares of trust units that invest in physical gold, silver, and platinum.

Market top

You never see offerings like this at market lows:

That’s right, according to numerous outlets, OpenAI is offering private equity firms guaranteed mid-teens returns in order to raise fresh capital. The deal offers a guaranteed return for co-investors like TPG and Advent. According to insiders, this is OpenAI’s latest push to attract capital as competitors have gained investor interest in recent months, potentially diverting capital once bound for OpenAI elsewhere. Reuters reported that OpenAI is offering a sweeter deal than rival Anthropic.

OpenAI and Anthropic are competing for partnerships with buyout firms that would allow them to quickly roll out their AI tools to potentially hundreds of private, established companies owned by buyout firms (the other portfolio companies of these PE buyout firms). This would boost the adoption of their models and encourage customer stickiness at scale.

We would warn our readers and investors to beware of market risks, especially in AI. An investment return guarantee from a private firm is unheard of and quite worrisome.

March 27, 2026

MacNicol & Associates Asset Management

What we are looking at next week

Download in PDF format: