BEACONS OF THE WEEK

The two main purposes of a Lighthouse are to serve as a navigational aid and to warn ships (Investors) of dangerous areas. It is like a traffic sign on the sea.

Eldred Rock Lighthouse, Alaska

This lighthouse was first lit in 1906. The lighthouse is 17 meters tall and has a range of 13 nautical miles. The lighthouse was decommissioned in 1973 but is under restoration under a non-for-profit which one day hopes to open a visitor center.

Tourlitis Lighthouse, Andros, Greece

This lighthouse was originally built in 1897. The current structure was built in the 1990s. The actual lighthouse is only 7 meters tall, but it sits on high rock where its focal height is actually 36 meters tall. The current lighthouse mimics a 19th Century lighthouse that was destroyed during World War 2.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations. *

Luxury retailer in turmoil

Burberry, a popular London-based luxury brand that sells clothing, bags, footwear, and accessories is in the news this week for all the wrong reasons.

The company has seen its share price listed on the London Stock Exchange crater over the last year by 65%. The stock is down 46% year to date and was down 17% on Monday alone.

The stock moved lower on Monday after it was announced that the company was suspending its dividend and they were firing its CEO effective immediately. As part of the earnings release for the quarter that ended June 29, 2024, Burberry announced they would report a loss through the first half of their 2024 fiscal year, citing the poor global economic environment as the driver of this contraction.

Burberry retail sales declined by 22% year over year. Burberry saw its sales decline in every major region in the world except for sales in Japan. The clothing brand said in its earnings release that the luxury market provides more challenges than previously forecasted.

Burberry’s new CEO has spent 33 years in the fashion industry and has previously been the CEO of Michael Kors, Coach, and Jimmy Choo.

We will have to see if the once iconic British clothing brand can regain its status and make a turnaround or if another retailer spoiled its brand and image that will never recover.

Bullish investors

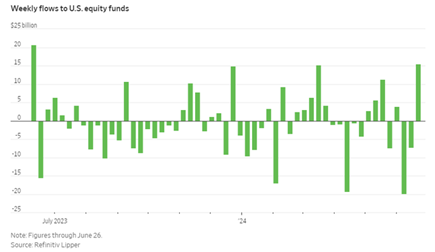

U.S. equity funds saw their largest weekly inflow in a year to the end of June. Over $15 billion in inflows in 1 week for U.S. equity funds was the highest since June 2023.

As stocks and indices hit new all-time highs, investors continue to pile into equity markets. Some of this cash that flowed into equity funds was more than likely in other asset classes including money market funds. Is this a sign of where markets move going forward? Or is it a sign that investors are chasing returns and have FOMO (fear of missing out)?

We are not surprised this inflow happened. As inflation continues to slow, the likelihood of rate cuts has increased, and markets continue moving higher. Investors do not want to continue missing out on the juicy returns equity markets have achieved over the last 18+ months.

We think this inflow could be a contrarian sign for investors as the melt-up reaches its final stages. Valuations have been stretched, market concentration has surged, earnings have slowed, geopolitical tensions have increased, and the economy is showing some serious cracks. We think now is the time to diversify and the time to have protection in place if markets do end up turning over in the next 6-12 months.

Huge commitment

Elon Musk seems to be completely turning his back on the Democratic party. The outspoken billionaire has in recent years shared more and more of his political opinions. On Monday, Musk committed $45 million a month until the election to a new super Trump PAC. Other backers of the megafund include Musk allies. Individuals include Palantir’s Co-Founder Joe Lonsdale and the Winklevoss twins.

This is a $180 million commitment from Musk and is something nobody would have predicted a decade ago. Trump and Musk have had a rocky relationship over the years. In early 2016 Musk said Trump was not the man for the job. Later that year, Musk was appointed one of Trump’s special advisors as he made the transition into the White House. A few months later, Musk cut ties with Trump over his green energy policies. Trump has also been critical of electric vehicles in the past. Fast forward a few years and the two exchanged compliments through the media. Trump was highly supportive of Musk during his feud with the California government. In 2022 Trump seemingly lashed out at Musk yet again. However, just 2 years later things seem well between the two billionaires.

However, we think this commitment from Musk has more to do with what the Democrats have done and less to do with Trump and the Republicans. Musk has consistently said the current administration has made repetitive mistakes, slowed the economy, and turned up the heat when it comes to division.

The commitment from Musk came on the same day as Trump’s Vice President pick. Trump picked a staunch supporter of him from the Senate, junior Senator JD Vance of Ohio. Vance is a former military member, Yale law grad, author, and venture capitalist. Whatever side of the aisle you sit on, you must admit that his resume is impressive.

Beyond that, Trump is now leading Biden in almost every swing state and within the margin of victory in a few historically blue states.

This comes a few days after the assassination attempt on former President Trump’s life.

For now, it seems like Trump and the GOP have all the momentum and that you should prepare your portfolio for a Trump victory and a GOP majority. His policies could be inflationary in their early days (ie. New tariffs).

Something has got to give

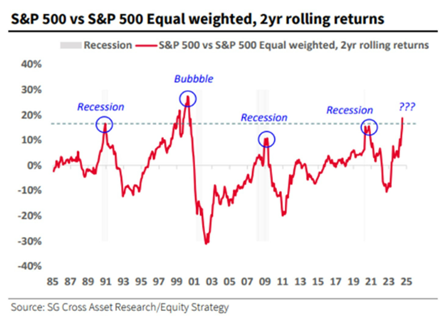

We ran by a chart from SG Cross Asset Research on X this week that set off some alarms for us.

The chart shows rolling returns for the S&P 500 versus returns from an equal-weighted S&P 500

The chart tracks the rolling returns of each asset class relative to the other. When the trend moves up, the S&P 500 outperforms. When moving downward, the equal-weighted index outperforms. Over the last 18 months markets have become as concentrated as ever and indices have been pulled along by mega caps and the Magnificent 7.

Over the last 40 years, the outperformance by the S&P 500 over the equal-weighted index on a rolling 2-year basis has only reached current levels twice before. The first occurrence proceeded to a recession and the second led to a major market bubble bursting.

We are not saying we are guaranteed a recession or a market bubble popping. We believe this outperformance is unsustainable and investors should pile into large caps that have lagged the Mag 7 and S&P 500, as well as consider buying small caps.

Large caps for the most part are at all-time highs, while small caps have severely lagged over the last few years and still have a lot of room to run. Small caps are also for the most part trading at discounts while many large and mega caps are trading quite expensively.

Small caps have also made some legitimate technical breakouts over the last 2 weeks which has caught the attention of many investors. Do not be surprised if small caps have a summer run after a few years of being beaten to a pulp.

Trump Presidency potential

A second Trump Administration could tap Jamie Dimon for Treasury Secretary in a move that has caught the attention of many. Dimon is the CEO of JP Morgan Chase and has been so since January 2006. Dimon is a global leader in the financial sector and has grown JP Morgan substantially since he began running the company.

After years of stagnation, JP Morgan’s stock has surged with Dimon at the helm.

We are not sure how Dimon will be as a Treasury Secretary but we applaud his skills as a leader and CEO. There are two things we have read about Dimon in the past weeks when it comes to policy to keep in mind if he becomes the Treasury Secretary. Dimon believes we should be close with India and admires their current Prime Minister Modi. He believes we should be more strategic with China and not treat them like an enemy. We know his background is not in foreign policy but perhaps he could have the ear of people in charge of foreign policy in a Trump administration. Just food for thought.

Despite being critical of Jerome Powell, Trump will also reportedly not look to remove Chairman Powell of the FED whose term ends as Chairman in 2026. Trump also reportedly believes the FED should not cut rates until after the election.

Tides changing

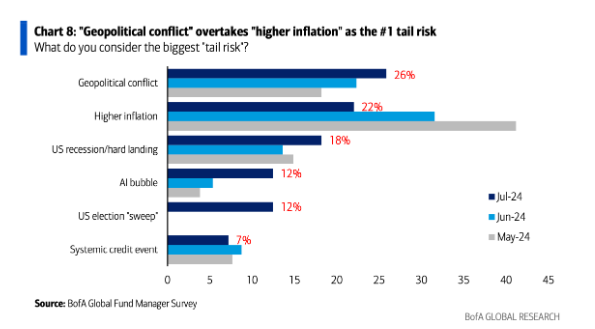

As inflation cools (for now), fund managers are now worried about something more than inflation for the first time in over a year.

According to the Bank of America Fund Managers Survey, the largest tail risk fund managers see is geopolitical conflict, followed by higher inflation. Just one month ago, the biggest risk was inflation by quite a large margin. Take a look at the graphic below.

We also have a new risk on the list that 12% of respondents think is the largest tail risk, an election sweep. After the debate and the media turning on Biden, polls suggest a Republican sweep in Congress and the Presidential race. Obviously, this much power for one party will make it easier to pass legislation and the GOP agenda but risks come with that as radical changes could potentially be made.

On the geopolitical front, we agree with many fund managers as the world currently has more conflict and tension than it has had at any other point over the last 5-10 years. There is a trade war and Cold War 2.0 between China and the U.S. Eastern countries and adversaries of the U.S. are cuddling up to each other and opposing the West. Russia has boldly invaded Ukraine. The conflict in Gaza and Israel has accelerated over the last 8-10 months. Houthis are attacking global ships in the Red Sea and Suez Canal. China is turning up the heat on Taiwan.

So how do you play this unpredictability where trade disruptions and conflict are likely? Hard assets will continue to be in demand as they have a strong store hold of value, as well as buying companies that can benefit from an uncertain environment.

Chip stocks struggle

Repeat what we wrote out loud. Can you believe it?

Shares of semiconductor companies and microchip stocks were under heavy pressure on Wednesday as new worries over China and Taiwan emerged.

The Biden administration reportedly told the Netherlands and Japan that it could invoke foreign product rules to limit sales to China in the semiconductor space.

At the same time, Trump told Bloomberg that Taiwan should have to pay the U.S. for its protection from China. The comments undermine current policy if China tries to retake Taiwan.

These comments by both parties sent microchip equipment makers lower like Tokyo Electron and ASML as well as the microchip supplier of Nvidia, Taiwan Semiconductor, and Nvidia and other chip stocks like AMD, Micron, and Broadcom.

The semiconductor industry and its suppliers and customers are firmly entrenched in the national security mindset. As the capabilities of these technologies expand, expect more trade disputes to occur which could impact sales down the road for these companies.

As of Wednesday morning, Nvidia shares were down 5.4% on Wednesday and 12% over the last 5 trading sessions. On top of the supply chain and geopolitical conflicts that are on the rise, Nvidia has been recently hit by the technology exodus from investors. Some investors have rebalanced after a strong first half from semiconductors and companies like Nvidia as well as mega-cap tech stocks in general. Investors are not the only ones pulling back on their semiconductor and tech exposure. Insiders at Nvidia have been selling throughout this year as have many insiders at large technology firms including Jeff Bezos who has now sold $10.25 billion in Amazon shares this year. Nvidia shareholders have sold much less but have sold $230 million worth of shares over the last week.

Nvidia’s CEO has recently said he is confident in Taiwan semiconductor’s geographical diversification with new sites under construction in Arizona and Japan.

The major beneficiary in the sector on this foreign uncertainty was the American firm Intel which saw its shares rise on Wednesday. However, Intel shares are down over 20% this year and have greatly underperformed its peers.

Consolidation in the steel industry

The steel industry continues to announce deals and potential consolidation. Late last year one of our major holdings, U.S. Steel announced it was being acquired by Japan’s Nippon Steel. The takeout offer is $55/share, a hefty premium from U.S. Steel’s share price before the announcement. In April 98% of shareholders voted in favor of the deal. The only remaining step for the $14.9 billion deal to go through is to pass through regulatory obstacles. The deal has drawn criticism from the United Steelworkers labor union which fears potential job loss. Regulators will also push back on the deal which is why U.S. Steel shares are trading well below that takeout price offer.

The deal is expected to close at some point this year. Nippon Steel has pledged there will be no job loss in the U.S. and many think there is hope for this deal as Japan is a strong ally of the U.S. Nippon Steel has even pledged that they will move their headquarters to U.S. Steel’s current HQ in Pittsburgh. Nippon Steel beat out other rivals Cleveland Cliffs, Nucor, and ArcelorMittal in acquiring U.S. Steel.

We have a little hope for this deal passing which is why we have held our shares in U.S. Steel. We also think even if the deal falls through that there is tremendous upside in the company as it trades at a discount and provides a vital product to the global economy. The company is also sought after by other U.S. producers who are willing to pay a premium to acquire U.S. Steel. Share prices are slightly above where they were before the deal announcement and are up 56% over the last year. We will continue to hold the company unless something seriously changes in the global economic environment.

We bring this all up because Cleveland Cliffs, who has pursued U.S. Steel for over a year pivoted and announced that they acquired the Canadian company Stelco for $2.5 billion. Cleveland Cliffs is the 2nd largest steelmaker in North America and is the largest seller of steel to the auto industry in the U.S. This move will reportedly diversify the company’s business and give them more exposure to customers who purchase steel on the open market.

The CEO of Cleveland Cliffs says he remains interested in U.S. Steel if the deal with Nippon Steel fails to meet regulatory requirements. Last August Cleveland Cliffs went public with their interest in U.S. Steel which initiated a bidding war between numerous steel giants for the acquisition of U.S. Steel.

Steel prices have slipped in recent months, but many analysts and industry experts expect prices to move up moving forward.

Cleveland Cliffs expects the deal to add to the company’s per-share earnings. The acquisition will also bring $120 million of estimated annual cost savings. The deal needs to pass through Canadian regulatory approval, but Cleveland Cliffs has already been in contact with them and expects no issues.

Deal-making in the steel industry continues to heat up and we are happy to be investors in the vital industry.

MacNicol & Associates Asset Management

July 19, 2024