Share This Post Today!

San Felipe Light, San Felipe, Mexico

This active lighthouse is located in the northern region of Baja, Mexico on the coast of the Gulf of California. The 72-foot-tall lighthouse has an adjoining 1 story keeper’s house. It is located in a town known for fishing with a small resort area. The city’s population is approximately 20,000.

Punta Arena de la Ventana Light, La Paz, Mexico

This lighthouse was built in 2009 and stands at 92 feet tall. The lighthouse replaced an original lighthouse which had to be removed. The site is open to tourists.

*Feel free to send us your photos of Lighthouses to be featured in our weekly market observations.

Peace and market hype?

On Sunday, major reports emerged that a peace deal had been agreed upon between the U.S. and Iran. This report comes after numerous attempts from both parties over the last few months to create a framework for a peace deal. On Monday morning, markets roared on this report, and the price of oil moved below $80 per barrel for the first time since the conflict began earlier this year. The Nasdaq pushed higher by more than 3% on this news as investors raced to buy risk-on assets. Treasury yields pulled back on this report as inflationary worries pulled back.

According to numerous sources, the two sides will come to a formalized agreement later this week. Beyond that, the two sides have also agreed to reopen the Strait of Hormuz. Trump posted on social media that ships are starting to move, many loaded up with oil out of the Strait on Monday morning. The closure of the Strait of Hormuz has been the main reason oil prices have remained elevated as a significant percentage of global oil exports normally flows through the Strait.

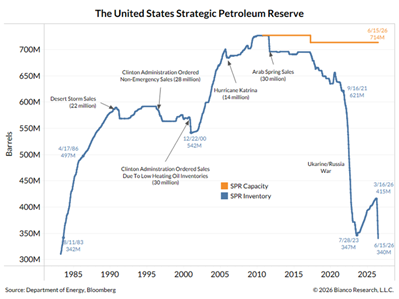

This agreement will alleviate inflationary pressures and potentially give the FED more time before rushing to hike interest rates to combat inflation. The agreement comes at a dire time as the U.S. strategic oil reserves sit at their lowest level in 42 years:

This peace deal has not changed our overall view on the energy trade in the long term. We still think prices will remain elevated, and the underlying oil and gas companies are still very attractive. Goldman Sachs’ research team published a revised energy forecast where they have lowered their oil price forecast due to the opening of the Strait from $90 per barrel to $85 per barrel. However, Goldman did state that the price forecast is heavily two-sided but is tilted to the upside for now. We will continue to watch the market very closely as supply will slowly come back online, with demand in select markets slowing in recent months, which could eventually change our view of the trade.

On Wednesday morning, just a few days after the peace deal was announced, Trump posted online that the deal is basically not finalized and the U.S. could resume “dropping bombs” on Iran, quite the statement for a peace deal if you ask us. This is a major reason why we will not be exiting the energy sector in size quite yet.

For now, it seems investors are once again all in on the momentum trade as the risk-on trend continues. This peace deal news comes just one trading day after SpaceX successfully IPO’d. SpaceX shares closed 19.6% higher on Monday, making it one of the largest companies in the world with a market capitalization of $2.5 trillion. SpaceX’s momentum is full on, and on Monday, underwriters exercised their overallotment option to sell an additional 83.3 million shares, raising another $11 billion. This overallotment reflects how strong demand was for SpaceX shares. Overallotment clauses in large IPOs are generally quite common and help brokers balance supply and demand. All of this Elon hype and IPO hype continued after hours on Monday and into Tuesday’s open as shares surged by more than 12% by 10 am EST. As of Tuesday morning, SpaceX’s market capitalization only trailed Nvidia, Apple, and Alphabet after surpassing the likes of Tesla, Microsoft, and Amazon.

Many investors pointed to this surge being led by the inequality in supply and demand for SpaceX shares. Obviously, there is a very strong demand for SpaceX shares as the IPO was highly anticipated, oversubscribed, and benefits from Elon Musk’s loyal followers. Index funds are also being forced to buy shares due to changes in index composition. On the other side, the company’s tradable float only represents 4% of shares outstanding. When you pair the two together, it’s no surprise that shares have rallied in early trading. Musk has created a scenario where share ownership is seen as lucrative (at least for now), and supply is extremely limited in the secondary market; it essentially creates a floor price for shares, at least for now. However, an issue could occur after 180 days when some SpaceX stock unlocks. After the company’s first quarterly earnings report, 20% of the stock will come off lockup, and it could be 30% if the stock is consistently above $175.

The demand for SpaceX shares is not only in domestic markets but also across the world. According to Bloomberg data, South Korean retail investors purchased a record $800 million in SpaceX shares on the first day of trading:

$800 million might not seem like a lot but in comparison to other speculative assets it is. South Korean investors bought $748 million in Micron shares over the prior 3 months. Micron has been the stock of the year and has seen mass inflows; SpaceX beat a 3-month number in a day. Beyond direct SpaceX exposure, South Korean investors bought $301 million in a space-linked ETF over the month prior to the SpaceX IPO. Quite the speculative bubble if you ask us.

It’s safe to say the return of momentum this week was led by both the peace deal and SpaceX this week. A perfect recipe for the return of risk on. We will state that the speculation could get worse as SpaceX options begin trading on Tuesday. Initial listings data indicate that SpaceX’s options will have strike prices ranging from $25 to $380. The first tranche of options will expire Thursday. After that, SpaceX’s options expirations will adhere to the standard monthly expiration cycle.

We will state that we did not participate in the IPO of SpaceX as we believe the valuation is way too expensive and price volatility will remain heavily elevated in the coming weeks, something we try to avoid. We did participate in a 2024 opening of SpaceX stock through one of our secondary Private Equity Partners. This relatively small position in SpaceX was bought from Insiders who were looking for liquidity. SpaceX stock is up 8x for us since then. We will be looking to exit shortly.

Not just SpaceX

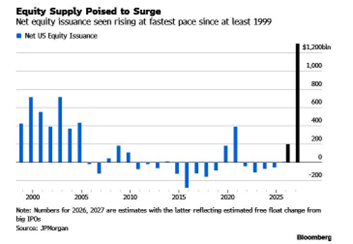

2026 has been a record year for equity markets. Net equity issuance is projected to hit its highest level since 1999.

Bloomberg points to the real test not being the debut of many names and issues but whether the market can continue absorbing this much issuance in a short period, especially over the coming months. For the last decade, a major feature of U.S. equity markets has been scarcity, as shares disappeared from the market through buybacks and go-private transactions.

The rush for capital does not stop with companies looking to go public; governments are looking to borrow right now, and public companies are looking for more capital. It’s essentially a rush for capital from all types of institutions.

We will not draw any definitive conclusions from the data above but warn investors that the above is likely not sustainable and the market potentially will not be able to absorb this much equity capital in a short period. If that is the case, many of these names that are issuing, and the broader market could see pullbacks a few months down the line.

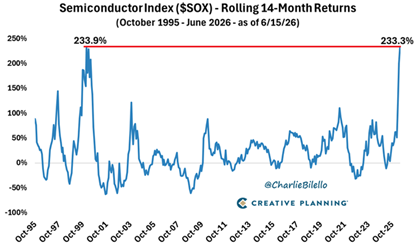

Equity issuance is not the only indicator that is at multi-decade highs; the semiconductor index (SOX) rolling 14-month return hit its highest level since February 2000 on Monday (another interesting chart from our friend Charlie Bilello). Over the last 14 months, it has been up over 230% as retail continues to chase hype, returns, and AI.

The ETF by iShares, which tracks the above index (SOXX), has seen its fund assets more than double over the last 3 months (talk about euphoria). The fund now has over $40 billion in assets. The trend is the same across the semiconductor industry.

Source: FactSet

Gold survey

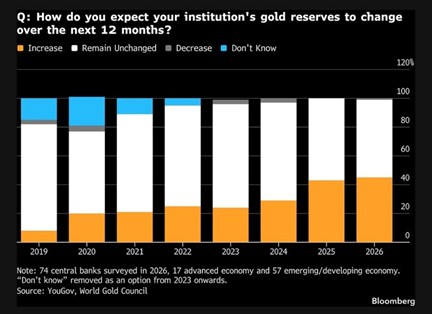

According to a 2026 survey of global Central Banks, 45% of the banks expect to increase their gold holdings over the next year, a large increase from the survey in 2019, when only 8% of respondents said they were looking to increase exposure to gold:

The survey was conducted by the World Gold Council and YouGov. The survey is also a key indicator that the thesis for the gold trade remains intact despite this year’s price pullback. Only one of the 74 Central Banks surveyed said they will cut their gold holdings this year. Of the banks that said they will be increasing their gold holdings this year, emerging market countries led the way. We think this is further evidence of countries looking to diversify away from traditional assets that are controlled by one country, like the U.S. dollar and the Euro. According to the survey, a few Central Banks are also moving their gold holdings home rather than storing them in the U.S. and UK. The survey states that fewer Central Banks are storing their gold metal in their vaults in London and New York than last year. We think this makes sense, especially with rising uncertainty, conflict in trade, and volatility in the White House. The French Central Bank moved the most gold away from U.S. vaults during the seven months ended January 2026. The UK remains the world’s largest holder of Central Bank bullion, holding gold for approximately 70 countries.

Many geopolitical experts have pointed to gold’s performance during times of crises being more relevant than ever moving forward due to the increased frequency of conflicts in recent years and instability in the global economy. Respondents of the survey mentioned above pointed to gold as a hedge for uncertainty and a portfolio diversifier in their long-term assessment of the precious metal.

We will also say that a peace deal would be bullish for gold as interest rate pressures ease with lower inflation worries.

We still like the metal in portfolios despite the price correction that we have seen in recent months. We continue to believe it remains a hedge against uncertainty and provides low-correlated returns to traditional markets. We also still really like many of the miners in the industry as their margins remain elevated despite the spot price pullback. Many of the large-cap names that we own all have sustainable costs of around or below $2,000/oz. Many of the names also remain at highly attractive multiples despite the market trading at elevated levels. Most of the larger miners that we own trade around 10-14 times forward earnings and continue to have strong margins.

Disclaimer: MacNicol & Associates Asset Management holds share of stocks, ETFs, mutual funds, and trusts that hold physical gold as well as equity instruments that invest in or operate gold mines.

Surprise, surprise

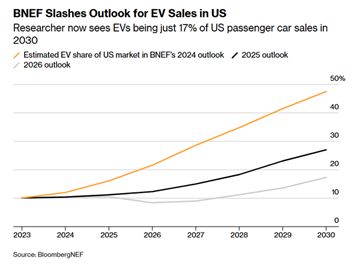

BloombergNEF released a report this week on electric vehicles, updating the previous year’s research. The new report outlines the demand for electric vehicles as a percentage of vehicle demand moving forward. The report states that 17% of U.S. passenger vehicle sales will be EVs in 2030; in last year’s study, the percentage was 27%. In 2024, the study projected 48% of vehicle sales to be from EVs. The study reveals lower adoption from consumers and a continued preference for traditional automobiles, which, for now, are generally priced lower in the U.S. market.

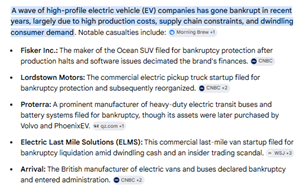

At this point, technology needs to prove itself to consumers. It’s a reason we avoided many of the EV names that were hyped up in 2021. Many of these companies went public at elevated valuations on the backs of being potential formidable competitors to Tesla. Since then, many of these stocks have seen their share prices collapse, and numerous of these firms have even filed for bankruptcy after destroying billions in shareholder capital.

The new-age pure EV companies have sunk over the last five years despite forecasting exponential growth and being extremely hyped. The lone outlier has been Tesla, which is, no pun intended, on a road of its own. In the end, many of these names destroyed billions in retail capital:

Source: FactSet

The new forecast from BloombergNEF comes after the Trump administration eliminated support for EV adoption by consumers. Under Trump, policymakers have moved to weaken fuel-efficiency standards, revoke California’s EV sales mandate, and eliminate a $7,500 federal tax credit for EVs. The researcher also lowered its EV sales estimates in China. China continues to dominate the global EV market, but growth is expected to slow in the coming years due to policy changes from the Chinese leadership.

We think the issues that the EV market is currently seeing will continue unless consumers pivot their thoughts on EVs and either accept higher prices or wait for EVs to drop in price. Batteries remain the main cost component of EVs, and in many markets, remain too expensive for BEVs to match combustion cars on price. While the push for battery supply chain localization is accelerating globally, matching China’s battery manufacturing costs remains a challenge.

What we are looking at next week

Markets enter the week of June 22nd with investors digesting a potentially meaningful shift in the macro narrative following last week’s Federal Reserve meeting. While the Fed left interest rates unchanged, new Chairman Kevin Warsh appears to have adopted a more hawkish tone, emphasizing persistent inflation risks and offering little indication that rate cuts remain on the horizon. Equity markets responded immediately in a negative way, with the S&P500 declining 100 points in the afternoon session. Treasury yields also moved higher as investors reassessed expectations for monetary policy.

Investors will also be watching whether enthusiasm surrounding the AI and tech complex can withstand higher rates and lofty valuations. SpaceX’s historic IPO has quickly become the new focal point for speculative capital, with shares continuing to climb after their debut, reinforcing investors’ appetite for transformative growth stories. Meanwhile development surrounding a potential U.S.-Iran peace agreement remain an important wildcard. While a deal was announced over the weekend, details have yet to emerge and given the ongoing instability and uncertainty around the region, the notion that a durable ceasefire or resolution will last remains an unknown.

MacNicol & Associates Asset Management

June 19, 2026

Download in PDF format: